Topic Paper 1 - RSE Structure and Profile

About this paper

This paper provides detail on draft "Superannuation Reporting Standards (SRS) 605.0 RSE Structure" (SRS 605.0)and "SRS 606.0 RSE Profile"(SRS 606.0).

The proposals in draft SRS 605.0 and SRS 606.0 will lay the foundation to collect more data at superannuation product and investment option levels and enhanced expense data. This will support the work APRA is doing to improve outcomes for superannuation members and increase its supervisory intensity on areas of the industry that are underperforming or where improvements in practices are needed.

As described in the "Superannuation Data Transformation Phase 1 Discussion Paper" released on 7 November 2019, this is the first paper in a series of Topic Papers.

This paper provides details of the proposed changes to reporting requirements regarding Registrable Superannuation Entity (RSE) Structure and Profile including:

Objectives of the proposed changes;

- The current state;

- Drivers for change;

- The proposed state, and;

- Specific areas of the proposals that APRA is requesting feedback on.

The proposals in this Topic Paper should be read in conjunction with the Discussion Paper "Superannuation Data Transformation" and the draft reporting standards SRS 605.0 and SRS 606.0.

Formal written submissions for Topic Paper 1 close on 17 January 2020. APRA will also be engaging with industry participants via round-table discussions and undertaking a pilot collection of the proposed data set out in the draft reporting standards. This will assist APRA to refine and finalise the draft standards, taking into account industry feedback and insights from the pilot data collection process.

Chapter 1: Introduction

1.1 Background

Over the last decade, the superannuation industry has grown in size and importance in the Australian economy, with total assets of superannuation entities increasing from $1.1 trillion to $2.9 trillion in assets. The evolution of the superannuation system has been accompanied by continued consolidation of RSE licensees and RSEs, with large and more complex entities managing the retirement benefits of most Australians. In this context it is critical that regulators and other stakeholders have access to data that appropriately reflects the size, nature and complexity of the industry.

A significant volume of data on the superannuation industry is already available, but there are important gaps in coverage and quality that need to be addressed in order to enable deeper insights into RSE licensee operations and provide a better understanding of their effectiveness, and the outcomes delivered to their members.

A key focus for Phase 1 of the Superannuation Data Transformation is to address coverage issues with the current data collection that will support the industry to implement the requirements in "SPS 515 Strategic Planning and Member Outcomes" (SPS 515) and support APRA’s work to improve transparency on RSE licensee and RSE performance. In particular, Phase 1 of the Superannuation Data Transformation will facilitate performance assessments for choice products and more granular performance assessment for MySuper products in key areas, such as expenses.

1.2 Drivers for change

Drivers for change for the Superannuation Data Transformation are outlined in the Discussion Paper "Superannuation Data Transformation" released on 7 November 2019.

For this topic RSE Structure and Profile, the drivers for change stem from the complexity of superannuation fund operations and structures, with funds comprising many components. To measure performance and outcomes successfully, APRA needs to have a clear and consistent picture of what these different components are, and how they relate to each other.

APRA’s data collection does not currently extend to all products and investment options beyond MySuper, and yet these represent a significant portion of the superannuation industry. The Productivity Commission’s review into the efficiency and competitiveness of the superannuation system1 recommended that APRA collect and publish member and performance data at the investment option level.

The proposals in SRS 605.0 and SRS 606.0 form the foundation to collect more granular data at product and investment option levels and facilitate assessment of member outcomes and performance of RSE licensees at these levels.

1.3 Objectives of the proposed changes

Through the changes proposed in this paper, APRA is seeking to;

- build a common data framework which fosters a complete and consistent classification of the different components that make up the structure of a superannuation fund;

- improve visibility of the different components of a fund and the relationships between them; and

- set the foundation to collect granular data in the future which will enable assessment of RSE licensee operations, performance and outcomes to members in different superannuation products and investment options.

1 The Productivity Commission undertook a review of the efficiency and competitiveness of the Australian superannuation system and its final report was released on 10 January 2019. More information can be found here: https://www.pc.gov.au/inquiries/completed/superannuation

Chapter 2. Proposed RSE structure and profile information

APRA is proposing to collect reference information on RSE structure and profile to inform each level of reporting for further data and provide additional visibility of the operations of the RSE.

This will include information on products and investment options, as noted above. To facilitate greater transparency on fees and costs, APRA also proposes to collect a new level of reporting known as an ‘Investment Menu’. The primary aim of this new level of reporting is to capture additional fees charged to gain access to certain investment options. Further details on this new reporting level is outlined below in section 2.2.

The data proposed for collection in SRS 605.0 and SRS 606.0 will provide a clear and consistent picture of the different components within a fund and the relationships between these components. The data will also provide the foundation upon which more granular and meaningful data can be collected to enable deeper analysis and insights.

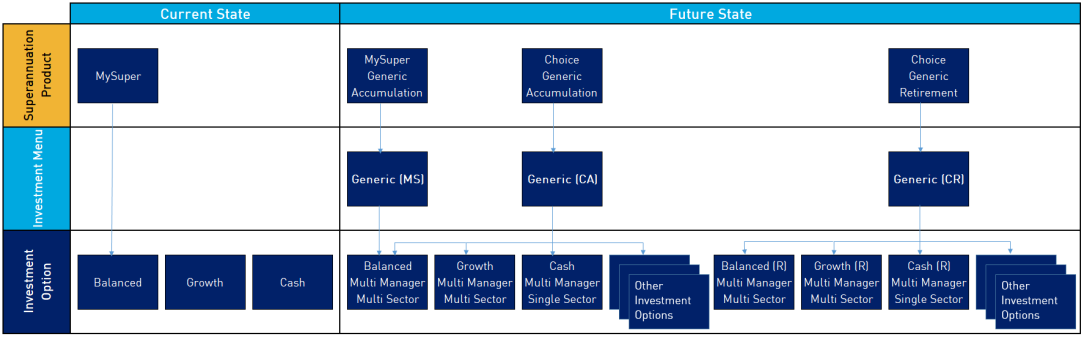

In SRS 605.0, it is proposed that each entity submit reference data for each product, investment menu and investment option. These reporting levels are described briefly below, with more detail available within draft SRS 605.0 which accompanies this Topic Paper.

SRS 606.0 proposes to collect the number of members in each product, investment menu and investment option and member assets in each combination of product, investment menu and investment option.

2.1 Superannuation Products

Existing requirements

Under the existing superannuation data collection, RSE licensees report data about and for MySuper products. RSE licensees also report data about and for defined benefit sub-funds.

Proposed changes

Under SRS 605.0 and SRS 606.0, a superannuation product is defined as a class of beneficial interest in a regulated superannuation fund.

APRA is proposing in SRS 605.0 to expand the data collection to cover all products to ensure full visibility across an RSE. Products have therefore been categorised into three ‘Product Types’: ‘Defined Benefit’, ‘MySuper’ and ‘choice’.

APRA is proposing in SRS 605.0 to collect data on all products within an RSE. Through SRS 606.0, APRA is proposing to collect the number of members in each product and the member assets in each combination of product, investment menu and investment option.

Whilst the use of the terms Defined Benefit and MySuper is well understood there is currently no agreed definition of a choice product. For the purpose of APRA’s reporting standards, APRA is proposing to define a choice product to be any product which is not a MySuper product or Defined Benefit product.

Definitions of products are not applied consistently across the industry. To enable consistency in the classification of what determines different products, APRA considers the following characteristics to be helpful:

- Product Type - as described above;

- Product Category –providing more detail of specific product types - such as insurance only, MySuper –material goodwill and MySuper – large employer;

- Product Phase – based upon the taxation status - including accumulation phase, retirement phase and transition to retirement phase; and

- Access Type – specifically how a member joins the product – including individual without an advisor, individual with an advisor, employer-linked (standard product or tailored product) or any combination of the above.

APRA acknowledges that for some RSE licensees these characteristics may already be used to classify a product.

APRA is seeking data from entities on the current suite of all products defined by RSE licensees and how they would map to the characteristics outlined above.

APRA seeks feedback from industry on the classifications outlined above including the definitions in the associated draft SRS 605.0 and specifically any products which don’t fit within these definitions.

2.2 Investment Menus

Existing requirements

The concept of an investment menu is a new reporting level and therefore does not exist under the current reporting requirements.

Proposed changes

Investment menus are defined as a group of investment options available to members in a product. This concept is primarily designed to capture where additional fees are charged in order for a member to gain access to particular investment options. Members in different products may have access to different investment menus comprising differing or overlapping investment options. In some cases, a member in a product may be able to gain access to an extended menu of investment options via the payment of an additional ‘platform access’ fee.

Furthermore, the same investment menu may be made available through more than one product. Complex RSEs may have multiple investment menus reflecting each of the different groupings of investment options available to members. Conversely, some RSEs, such as those with a single product, may only have a single investment menu.

APRA is proposing in SRS 605.0 to collect data on all investment menus within an RSE. Through SRS 606.0, APRA is proposing to collect the number of members in each investment menu and the member assets in each combination of product, investment menu and investment option.

Lifecycle investment strategies

A lifecycle investment strategy is one in which the asset allocation varies for a beneficiary or member according to factors such as their age and/or the time remaining to retirement. Currently for MySuper products with a lifecycle strategy, the information on the overall lifecycle investment strategy including the glide-path information as well as the characteristics which determine each cohort or lifecycle stage are reported at the product level. Characteristics and performance for each lifecycle stage or cohort are reported at the investment option level. This approach works for MySuper products as there is only one investment option for each product.

For choice products there is typically not a one to one relationship between the product and the investment option. To cater for the added complexity of lifecycle investment strategies existing in choice products, APRA is proposing that the overall lifecycle strategy information is reported at the investment menu level, including the glide-path information and characteristics which determine each cohort or lifecycle stage. Each lifecycle stage or cohort will be reported at the investment option level.

For an illustration of the reporting population and levels APRA proposes and a comparison with the existing reporting population and levels, including an example with a lifecycle strategy, refer to Appendix I.

APRA is therefore proposing to collect data on the following type of investment menus:

- Platform;

- Lifecycle Strategy option; and

- Generic (to capture all other investment menus).

2.3 Investment options

Existing requirements

In the existing superannuation data collection, data is collected for MySuper investment options on a limited basis and more detailed information for select investment options (SIO). As set out in the discussion paper, not having adequate information about all investment options is insufficient for APRA, industry or other stakeholder needs.

Proposed changes

APRA is therefore proposing that data is reported for each investment option available to members within the RSE through SRS 605.0.

Through SRS 606.0, APRA is proposing to collect the number of members and the member assets in each investment option.

An investment option will typically be the lowest level of investment product that a member will have the option to invest in.

Investment option reporting is also proposed to capture Annuities for completeness.

APRA notes that the same investment option may be made available through more than one investment menu.

For an illustration of the reporting population and levels APRA proposes and a comparison with the existing reporting population and levels, please refer to Appendix I.

Reporting of direct investments

There are several specific direct investments that APRA proposes to be reported as investment options. However reporting on each of these at an individual level is not considered necessary for the objectives of this data collection. APRA is therefore seeking reporting on direct investments at a collective level, based on those direct investments which have a common fee structure, investment option category and description in related disclosure. An example would be the option for members to invest in individual shares on an index. In this example, the collective shares would be reported as one investment option named ‘ASX 300 – individual shares’, together with the number of shares.

Other direct investments, such as ETFs and LICs, are proposed to be reported individually as these are individually vetted by the RSE licensee. Term deposits are proposed to be reported individually by duration and provider. Further information on the reporting of direct investment option categories can be found in the instruction guide for the reporting form SRF 605.0.

2.4 Unique identifiers

Existing requirements

Currently under "SRS 001.0 Profile and Structure (Baseline)", the RSE licensee must provide a Unique Identifier (UI) for each MySuper product, defined benefit sub fund and SIO for each RSE.

Proposed changes

APRA proposes to extend this principle to all investment options. Similarly, RSEs will be required to provide UIs for all superannuation products and all investment menus.

Industry-wide UIs are either not currently available, or do not provide the required level of granularity to meet APRA’s needs.

Where possible, entities should re-use unique identifiers that have previously been used in reporting for "SRS 001.0 Profile and Structure (Baseline)" (SRS 001.0). Lifecycle stage identifiers and select investment option identifiers should be reused as an investment option number under the proposed SRS 605.0. Similarly the MySuper identifier on SRS 001.0 should be reused as a Product number on the proposed SRS 605.0.

2.5 Member and account relationships

Existing requirements

In the existing superannuation collection, the number of member accounts and the sum of member balances is collected at the defined benefit sub-fund, MySuper product and lifecycle stage, and select investment option levels via "SRS 601.0 Profile and Structure".

In the current data collection only the total number of investment options which are not MySuper or Select Investment Options is collected. No additional data about these options is collected. No data on member accounts and balances is collected for choice products, and there is no data on which investment options are available through each choice product.

Proposed changes

SRS 606.0 proposes to collect the sum of member assets and number of member accounts for each combination of product, investment menu and investment option.

The member assets will not be collected separately for each product and investment menu as these can be derived from the product, investment menu and investment option combination. The number of member accounts will also be collected at the product and investment menu levels, as these cannot be derived due to members being invested in multiple investment menus and investment options.

2.6 Overlap with current reporting standards

There is a degree of overlap between data to be collected through the proposed SRS 605.0 and SRS 606.0 and data collected under existing reporting standards.

To the extent that the new forms would duplicate data already collected, APRA will consider exemptions from specific items on existing forms, or where relevant the discontinuance of collection of an entire form.

Chapter 3. Proposed non-confidentiality determination

APRA’s Superannuation Data Transformation will lead to significant changes to the reporting requirements. As a result of these changes, APRA needs to consider whether the data reported under FSCODA should be determined to be non-confidential and publically accessible.

APRA is generally able to publish aggregate industry-level data without restriction. To achieve the objectives of the enhanced superannuation data collection, which include improved accountability of the industry and more informed analysis and assessment of the performance of the superannuation industry by stakeholders, it will be necessary to publish data at an individual entity, product and investment option level.

Under section 56 of the APRA Act, data reported to APRA under FSCODA is protected information and generally not able to be disclosed at an entity level, unless APRA determines the data to be non-confidential.

However section 57 of the APRA Act permits APRA to make a determination that data provided in a particular reporting document, which has been submitted in accordance with a reporting standard made under FSCODA, is non-confidential if it considers the benefit to the public from the disclosure outweighs any detriment to commercial interests that the disclosure may cause.

FSCODA also requires that APRA must not make such a determination unless it has:

- given interested parties (bodies or associations representing the relevant kind of financial sector entity) a reasonable opportunity to make representations as to whether information of the kind that is proposed to be released is confidential; and

- taken any such representations into account.

APRA proposes to determine under section 57 of the "Australian Prudential Regulation Authority Act 1998" (APRA Act) that all data under SRS 605.0 and SRS 606.0 is non-confidential.

Data which APRA determines to be non-confidential will identify individual entity data but will not breach the privacy of individual members. The scope of proposed publication of data and treatment of privacy protection in public data releases will be set out in the final Topic Paper release of Phase 1.

Reasons for the proposed determination

The data to be collected under SRS 605.0 and SRS 606.0 will provide essential foundational material to fulfil the objectives of the Superannuation Data Transformation. It will provide the necessary information on RSE structure which will enable more meaningful assessment of performance and outcomes for members in different products and investment options, ultimately supporting initiatives to improve outcomes for superannuation members.

3.1 Feedback sought on confidentiality proposals

To assist APRA in making its decision about the data to be determined non-confidential, submissions from RSE Licensees and other interested parties that seek to have data remain confidential should include specific:

- details of the data items that should remain confidential;

- information on how the disclosure of that information would lead to detriment to member interests, and the extent to which that could occur, and/or;

- information on how the disclosure of that information might lead to detriment to RSE Licensees or other parties’ commercial interests.

Chapter 4. Consultation questions: RSE structure and profile

Comment is invited on the content of this paper, specifically in the below areas:

Questions

- Are the characteristics outlined for products in the proposed reporting standards useful and practical for defining separate products or divisions?

- Is the concept of investment menu useful? Are there fees charged by the RSE Licensee at this level?

- The draft SRS 605.0 seeks to broaden the scope of investment options included in reporting. Are there any areas of particular concern, gaps or areas requiring further clarification in SRS 605.0?

- The draft reporting standards that accompany this Topic Paper contain concepts and definitions that differ from the existing suite of reporting standards. Are there any products, investment menus, investment options or other levels of reporting which do not fit these new definitions? Are there any gaps or areas requiring further clarification?

- Are there existing industry wide unique identifiers that would be preferred to funds maintaining a list of unique identifiers for superannuation products, investment menus and investment options?

- Feedback as outlined in item 3.1 "Feedback sought on confidentiality proposals".

4.1 Submission of responses

Written submissions should be sent to superdatatransformation@apra.gov.au by 17 January 2020 for Topic Paper 1 (RSE Structure and Profile), and as advised for subsequent topic papers. Address submissions to:

General Manager

Data Analytics & Insights

Risk and Data Analytics Division

Australian Prudential Regulation Authority

GPO Box 9836

SYDNEY NSW 2001

4.2 Submission of pilot data

Through Phase 1 of the Superannuation Data Transformation, APRA is seeking to collect pilot data to test and inform areas for clarification prior to finalising Phase 1 reporting standards. As the pilot data is based on draft reporting standards, this data is not collected under the auspices of FSCODA and will be on a best endeavours basis.

Each Topic Paper will be accompanied by draft reporting standards, a reporting template to collect pilot data, specified reporting periods for RSE Licensees to provide data for in the template and due dates for submission.

Following the collection of the Phase 1 pilot data, an updated data template will be provided to entities for completion to further test and clarify the draft reporting standards.

Following the first data collection after the Phase 1 Reporting Standards have been finalised, APRA intends to publish this data. It is intended that the released data will assist RSE Licensees in meeting their obligations under SPS 515. It will also inform Phases 2 and 3 of the Superannuation Data Transformation.

This table summarises the key features of the initial pilot data collection for this topic paper:

| What is required? | Use best endeavours to complete the reporting template according to the instructions provided. |

|---|---|

| Reporting Entities | All RSE Licensees are to provide information for each product, investment menu and investment option they offer. |

| Reporting period | As at 30 November 2019. |

| Due date | 17 January 2020. |

| Where to submit? | Via SecureDoc. Submitting entities will be provided with a template and instructions by APRA. |

| Any queries? | Via email superdatatransformation@apra.gov.au. |

Appendix I – Illustration of the reporting population and levels

Example I – current reporting vs. future state under the proposals in SRS 605.0.

Example II - Illustration of reporting for a MySuper product with a lifecycle strategy under the proposals in SRS 605.0.