Response to consultation - Interest rate risk in the banking book for Authorised Deposit-taking Institutions

Executive summary

Interest rate risk in the banking book (IRRBB) is the risk to capital and earnings resulting from changes to the interest rate environment. Movements in interest rates impact the present value of future cash flows and the economic value of an authorised deposit-taking institution's (ADI) assets and liabilities, as well as income and expenses that are sensitive to interest rates.

IRRBB is a material risk to ADIs in Australia, given their balance sheets are generally concentrated in housing loans, retail deposits and high-quality liquid assets. ADIs must appropriately manage the underlying risks associated with changing interest rates and their balance sheet positions to ensure they can continue providing banking services to the Australian economy.

The recent international banking turmoil has highlighted the importance of adequate IRRBB risk management. In March 2023, three US regional banks failed largely due to poor IRRBB risk management that was exposed through recent changes in the interest rate environment.1 The failure of these banks emphasises the importance for ADIs in Australia to effectively manage their interest rate risks and their balance sheet positions.

APRA requires internal ratings-based (IRB) ADIs to hold capital against their IRRBB, which incentivises ADIs to hedge their interest rate exposures. This differs from other jurisdictions where a simple supervisory add-on to capital may be applied for this risk. Prudential Standard APS 117 Capital Adequacy: Interest Rate Risk in the Banking Book (APS 117) sets out APRA’s prudential requirements for ADIs in relation to the management and measurement of IRRBB and the holding of regulatory capital against this risk.

Review of APRA’s prudential standard for IRRBB

APRA has undertaken multiple rounds of consultation on its proposals to reform its IRRBB requirements. APRA’s most recent consultation in November 2022 aimed to achieve three key objectives:

- reduce some of the volatility in the IRRBB capital charge, as has been evidenced through recent market conditions;

- create better incentives for ADIs in managing their IRRBB risk, including raising standards of governance and the measurement of risk; and

- simplify and remove complexities in the IRRBB framework, including incorporating changes from the Basel Committee on Banking Supervision’s (Basel Committee) IRRBB standard.

APRA received seven submissions to the November 2022 consultation, five of which were confidential, and engaged with market participants through industry workshops and bilateral discussions. This Response to submissions paper sets out APRA’s response to feedback received in the November 2022 consultation. It covers a range of technical issues relating to IRRBB, including APRA’s requirements around the management and governance of IRRBB and the use of internal models to calculate IRRBB capital.

APRA’s updated proposed revisions to APS 117 finalise the calibration of the standard. In particular, APRA has addressed previously raised concerns on the treatment of embedded gains and losses and the observation period for the capital charge methodology. These revisions are expected to reduce volatility in the IRRBB capital charge compared to the current framework.

APRA has released the updated draft of APS 117 alongside this paper, which will be finalised in 2024 and come into effect from 1 October 2025.

IRRBB Capital Impact

The revised APS 117 is expected to materially reduce the IRRBB capital charge across IRB ADIs compared to the proposals set out in the November 2022 consultation. APRA expects ADIs’ IRRBB capital charge to be closer aligned with the capital charge under the current APS 117.

The revised APS 117 capital charge methodology will also reduce volatility in IRRBB capital requirements compared to the current framework. With these policy changes, APRA expects IRRBB capital to typically operate between 5-7 per cent (across the major banks) of Total risk-weighted assets (RWA), based on current banking book portfolios.

Requirements for non-Significant Financial Institutions (non-SFIs)

The recent international banking turmoil has shown that IRRBB poses risks to the financial soundness of all ADIs. In response, APRA is undertaking a narrow consultation on extending certain requirements of the prudential standard to also capture non-SFIs. This will require all ADIs to manage IRRBB commensurate with their nature, scale, and complexity.

These proposed requirements are intended to be proportionate and clarify existing requirements: they principally reaffirm APRA’s expectations that all ADIs need to manage their material risks, including IRRBB, as required by the existing Prudential Standard CPS 220 Risk Management (CPS 220).

APRA will undertake a three-month consultation on these requirements, before finalising them in 2024. The requirements would become effective as part of the new APS 117 in 2025.

Next steps

Next steps will involve:

- consulting on guidance – the draft Prudential Practice Guide APG 117 Capital Adequacy: Interest Rate Risk in the Banking Book (APG 117) has been released for consultation alongside this response paper, and will be finalised in 2024;

- requirements for non-SFIs – the draft requirements that will apply to non-SFIs are provided in Chapter 3 of this response paper, for consultation, and will also be finalised in 2024; and

- updating reporting requirements – the draft Reporting Standard ARS 117.0 Repricing Analysis and draft Reporting Standard ARS 117.1 Interest Rate Risk in the Banking Book will be released for consultation along with this response paper.

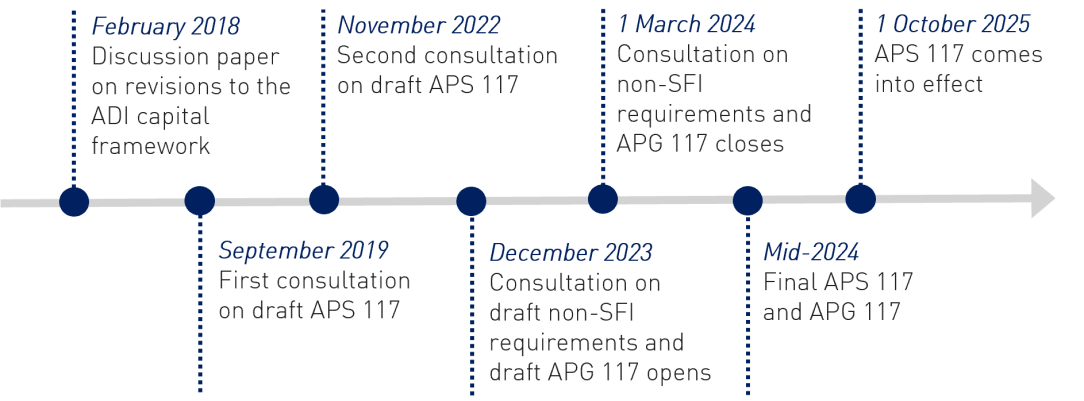

A timeline of the reforms to APS 117 is provided below.

Figure 1. Policy development roadmap for APS 117

Glossary

| ADI | Authorised Deposit-taking Institution |

|---|---|

| APRA | Australian Prudential Regulation Authority |

| APS 117 | Prudential Standard APS 117 Capital Adequacy: Interest Rate Risk in the Banking Book |

| Banking book item | An on-balance sheet asset, liability or equity item that is not part of an ADI’s trading book, not deducted from an ADI’s Common Equity Tier 1 (CET1) capital and not included in an ADI’s CET1 capital; or an off-balance sheet position that alters an ADI’s exposure to interest rate risk and is not part of the ADI’s trading book. |

| Basel Committee | Basel Committee on Banking Supervision |

| Basis risk | The risk of loss in earnings or economic value of the banking book arising from imperfect correlation in the adjustment of interest rates earned and paid on different instruments with otherwise similar repricing characteristics. This may arise from differences between the actual and expected interest margins on banking book items, where ‘margin’ means the difference between the interest rate on the items and the implied cost of funds for those items. |

| Calculation date | The date with reference to which an ADI’s IRRBB capital charge is calculated, such that the exposures and observations of interest rates used in the calculation are recorded at the close of business on that day. |

| Cross currency basis risk | The potential risk or uncertainty associated with the basis or spread between interest rates of two different currencies. It arises when there is a discrepancy or misalignment between the interest rates of two currencies in the foreign exchange market. |

| Embedded gains and losses (EGL) | The gain or loss arising from past movements in interest rates that have not been recognised in accounts. |

| Expected shortfall | An ADI’s prospective IRRBB capital charge is the ADI’s estimate of a 97.5 per cent expected shortfall of the prospective loss. The percentage expected shortfall is the expected loss conditional on the loss being in the worst 2.5 per cent of potential losses. |

| Foreign ADI | Has the meaning given in section 5 of the Banking Act. |

| Gap risk | The risk that arises from the term structure of banking book instruments and describes the risk arising from the timing of interest rate changes associated with these instruments. |

| IRB ADI | An ADI which has been approved by APRA to use the internal ratings-based approach to credit risk. |

| Non-significant financial institution (non-SFI) | An APRA-regulated entity, such as an ADI or its authorised non-operating holding company (NOHC), that is not a significant financial institution. |

| Optionality risk | The risk of loss in earnings or value due to cash flows varying from what an ADI had assumed, caused either by customers exercising stand-alone or embedded options differently from how the ADI had assumed they would, or by the operation of caps, floors and similar mechanisms that automatically adjust interest payments. |

| Repricing risk | The risk of loss in earnings or economic value caused by a change in the overall level of interest rates. This risk arises from mismatches in the repricing dates of an ADI’s banking book items. |

| Significant financial institution (SFI) | An ADI (that is not a Foreign ADI) or authorised NOHC that has total assets more than AUD 20 billion, or determined as such by APRA, having regard to matters such as the complexity in its operations or its membership of a group. |

| Single currency basis risk | The potential risk or uncertainty associated with the basis or spread between two interest rates denominated in the same currency. It arises when there is a discrepancy or misalignment between the interest rates of two financial instruments that are denominated in the same currency but have different underlying reference rates. |

| Yield curve risk | The risk of loss in earnings or economic value caused by a change in the relative levels of interest rates for different tenors (that is, a change in the slope or shape of the yield curve). Yield curve risk arises from repricing mismatches between assets and liabilities. |

Chapter 1 - Response to submissions

This chapter outlines APRA’s response to feedback on the five proposals set out in the November 2022 consultation on APS 117, which were designed to reduce volatility in the IRRBB capital charge calculation as well as create better incentives for ADIs in managing their IRRBB. APRA’s responses incorporate feedback from the consultation process and considers the recent international banking turmoil that resulted from poor IRRBB risk management. Additional issues raised in consultation are summarised in Table 1.

1.1 Treatment of embedded gains and loss

Under the current APS 117, embedded gains and loss (EGL) is an input in the IRRBB capital charge calculation. In November 2022, APRA proposed removing EGL from the IRRBB capital charge calculation in APS 117 and instead treating embedded loss as a regulatory adjustment, i.e. a CET1 capital deduction under Prudential Standard APS 111 Capital Adequacy: Measurement of Capital (APS 111). This proposal aimed to ensure a more stable IRRBB capital charge by reducing the volatility created from including embedded gains.

Comments received

Submissions raised concerns with APRA’s proposal to no longer recognise embedded gains in the IRRBB framework.

Submissions argued that not recognising embedded gains in the IRRBB capital charge creates an asymmetrical treatment and does not account for gains or losses on the effective cash flow hedge reserve items that have been removed from APS 111. Including EGL in the IRRBB capital charge would ensure the IRRBB framework recognises ‘real’ gains in the same way it recognises ‘real’ losses.

Submissions also highlighted that treating EGL as a capital deduction under APS 111 may lead to unintended consequences across the prudential framework, which are summarised below:

- Binding capital floor – when an embedded loss, removing EGL from the IRRBB capital charge reduces the total value of RWA measured under the IRB approach relative to RWA measured under the standardised approach. This increases the likelihood of a binding capital floor. Under APRA’s capital framework, the capital floor was only intended to be a backstop rather than a permanent binding constraint on a system-wide basis;

- Impact on related entities requirements – treating EGL as a capital deduction would increase the amount of capital required to be held for an ADI’s investment in a New Zealand subsidiary, as it could exceed 10 per cent of an ADI’s CET1 capital. This may lead to greater volatility in Level 1 capital ratios;

- Changes in the accounting treatment of banking book items – APRA’s proposal to treat EGL as a capital deduction is asymmetric as it only recognises embedded losses. Embedded gains are not recognised when treating EGL as a CET1 deduction. This could result in differences in capital outcomes depending on whether ADIs choose to measure a financial item at amortised cost or fair value for accounting purposes; and

- Leverage ratio – treating embedded loss as a capital deduction reduces the overall level of Tier 1 capital. This in turn reduces an ADI’s leverage ratio.

APRA response

APRA recognises the concerns raised and notes the unintended consequences of including embedded loss as a capital deduction rather than as an input in the IRRBB capital charge calculation.

In response, APRA has retained EGL in the IRRBB capital charge calculation and will now require senior management to notify its Board, and APRA, where the embedded gains component of the capital charge is material. This notification should include how the ADI is mitigating associated risks of a material embedded gain in their IRRBB capital charge. APRA also expects an ADI to consider the materiality of the embedded gains in its Internal Capital Adequacy Assessment Process (ICAAP).

1.2 Earnings offset

The earnings offset is an adjustment for the impact of interest rate changes on economic-value based earnings over a one-year holding period. Under the current APS 117, an earnings offset is calculated as part of estimating the impact of changes to the economic value of the banking book.

APRA had observed that the current setting of a one-year earnings offset does not bear any material outcome on ADIs’ choice of banking book profile or balance sheet management strategy. As part of the November 2022 consultation, APRA sought feedback on whether it should remove the earnings offset or maintain the current setting of having a one-year earnings offset.

Comments received

Submissions noted that removing the earnings offset would materially increase the absolute level and volatility of the IRRBB capital charge, which is counterintuitive to the policy objectives of the review of APS 117.

APRA response

In response to feedback received through the consultation process, APRA has decided to retain the one-year earnings offset. This aligns with APRA’s objective to not materially increase IRRBB capital requirements across the system. APRA does not support setting an earnings offset greater than one-year.

1.3 Stressed period

An IRB ADI is required to collect data to model and calculate their IRRBB capital charge. APS 117 requires ADIs to use interest rate data from an observation period of eight years.

In November 2022, APRA proposed demarcating this eight-year observation period into a one-year stressed period and a seven-year latest data period. The inclusion of this one-year stressed period was expected to reduce the volatility in an ADI’s IRRBB capital charge as the choice of stressed period would be the period that results in the highest prospective IRRBB capital charge based on an ADI’s current banking book portfolio composition.

Comments received

Submissions argued that although the proposal to demarcate the eight-year observation period may reduce volatility, it would also likely overestimate the IRRBB capital charge. This is because the one-year stressed period, which typically coincided with the Global Financial Crisis (GFC) period, resulted in a material increase in IRRBB capital outcomes compared to current levels.

APRA response

APRA is now demarcating the eight-year observation period into the concatenation of a 3.5-year fixed observation period that spans January 2020 to June 2023 and a rolling 4.5-year observation period that incorporates the latest data excluding the fixed observation period.

This means that until March 2028 reporting period, the observation window will be the latest eight years. Thereafter, this will change – for example in June 2028 the observation window will include the 3.5-year period January 2020 to June 2023 plus the 4.5-year period January 2024 to June 2028. This approach is preferable given the fixed-observation period encompasses interest rate increases, decreases and appropriate levels of interest rate volatility, and reduces concerns using the GFC as the stressed period.

1.4 Observation period and data frequency

The current APS 117 requires ADIs to update the frequency of the observation period on a quarterly basis. As part of the November 2022 consultation, APRA proposed moving this requirement from quarterly to annually, given this better aligns with the annually measured stressed period and was designed to reduce the operational and computational burden on ADIs. Additionally, this would remove the quarter-to-quarter volatility in the IRRBB capital charge due to movements in interest rates.

Comments received

Submissions noted that this proposal may create operational challenges and undue complexities in the IRRBB framework. This included impeding comparability of the IRRBB capital charge across ADIs if they update their observation periods at different times throughout the year and that existing quarterly processes are already established for capital reporting.

APRA response

APRA has reverted to the September 2019 proposal to require ADIs to update the observation period data to quarterly, rather than annually. This approach improves the risk sensitivity of the IRRBB framework, improves comparability in the IRRBB capital charge between ADIs and removes undue operational complexities.

1.5 Banking book profile

APRA proposed to strengthen some of the qualitative IRRBB requirements around governance, oversight, risk management and controls of an ADI’s choice of the maturity profile for shareholders’ equity. This involved requiring the setting of a choice of maturity profile for shareholders’ equity to be seen as a strategy that is set and approved by the ADI’s senior management, consistent with the risk appetite for IRRBB set by the Board, and not just seen as an assumption that ADIs set.

Submissions were supportive of this proposal and the amendments have been retained in APS 117.

1.6 Other issues

In addition to feedback on the five issues APRA consulted on in November 2022, submissions provided additional feedback on other areas of the IRRBB framework. The table below summarises this feedback and provides APRA’s response.

Table 1. Other issues raised in consultation

| Issues | Comments received | APRA response |

|---|---|---|

| Limited consideration to system stability | Submissions suggested that APS 117 does not provide enough consideration to earnings volatility risk and primarily uses the risk of a fall in economic value of the banking book as the key driver to calibrate capital requirements. Submissions stated this approach is inconsistent with other jurisdictions.

| APS 117 utilises an economic value of equity-based approach which capitalises the risk of loss arising from adverse movements in the economic value of the banking book due to the interest rate changes. APRA adopts a Pillar 1 approach for the capitalisation of IRRBB. However, other jurisdictions do not adopt a Pillar 1 approach and instead, under a Pillar 2 approach, have a monitoring framework and supervisory outlier test based on changes to the economic value of equity of banking book items. |

| Approach to capitalisation of spread risk and scope of market-related items | Some submissions suggested that APS 117 disproportionately allocates capital to liquid asset portfolios for the calculation of spread risk e.g. Australian Government and Semi-government securities that are hedged with interest rate swaps compared to other components in the capital framework (e.g. business loans). As such, it was suggested that APRA change the scope of market-related items from “all securities in the banking book” to “all securities designated at fair value in the banking book”. | Market-related items are to encapsulate all securities and not just items that are designated at fair value for accounting purposes. The recent US banking turmoil and collapse of SVB highlighted the potential pitfalls from not appropriately capitalising unrealised losses on liquid assets and designating securities at amortised cost. The APRA IRRBB capital framework, through its capitalisation of spread risk, has ensured that banks remain unquestionably strong to adverse movements in interest rates and that unrealised losses are appropriately capitalised. |

| Disproportionate capital requirements | Submissions suggested that capital requirements under APS 117 are mostly driven by the duration of equity and are disproportionate to the underlying risk. | APRA has strengthened requirements in APS 117 to improve the transparency of this strategy with Senior Management and the Board. Capital allocation issues have been addressed through changes made to the stressed period (and observation period) requirements for the IRRBB capital calculation. |

| Core deposits | Some submissions consider that the scaling factor of 0.9 applied for optionality risk is duplicative with the 90 per cent cap applied to the maximum proportion of core deposits and suggest removing the 0.9 scalar applied for non-rate sensitive deposits. | APRA does not consider a change is warranted. The 0.9 scalar behavioural assumption deals with core deposit withdrawal optionality risk whilst the latter accounts for a standardised assumption placed on the gap profile, which is captured in the prospective IRRBB capital charge. |

| Valuation of non-market related items | Submissions suggested that APS 117 includes requirements that are not consistent with ADIs’ internal funds transfer policy, and therefore make the requirement that discounted cash flow of non-market related items are equal to the purchase value at inception difficult to meet. Submissions have commented on several instances where it is difficult to achieve this. | APRA has made changes to APS 117, changing the requirement that they must be “equal to" to “must not be materially different”. |

| Complexity and timelines of implementation | Submissions requested that ADIs will need at least 18 months to implement the new IRRBB framework following the finalisation of APS 117. | APRA has delayed the implementation of APS 117 from 1 January 2025 to 1 October 2025. This provides the industry with the implementation time requested. |

Chapter 2 - MPA alignment

This chapter explains how APRA has updated APS 117 to align with its core strategic priority to Modernise the prudential architecture (MPA).2 In updating its prudential framework, APRA intends to deliver a clearer, simpler, and more adaptable framework that reduces costs, is easier for industry to understand, and is more efficient to supervise and maintain.

A key element of MPA is better regulation. This entails simplifying the design of APRA’s regulatory framework to make it more cohesive, proportionate to the size and complexity of regulated entities, and better aligned to the needs of its users. APRA has incorporated considerations of MPA into the updated draft of APS 117 to meet this purpose.

Avoiding duplication with CPS 220

CPS 220 is a cross-industry prudential standard that sets out requirements relating to the risk management framework of an APRA-regulated institution. These requirements include the need for an APRA-regulated institution to have a risk management framework that is consistent and integrated with the risk profile and capital strength of the institution, supported by a risk management function and subject to comprehensive review.

IRRBB is a material risk for the purposes of CPS 220 and therefore all ADIs, including non-SFI ADIs, must meet the risk management requirements set out in CPS 220 with respect to IRRBB. The draft APS 117, released for consultation in November 2022, included IRRBB management framework and governance requirements for SFI ADIs. Some of these requirements reiterated risk management requirements set out in CPS 220, which APRA would expect all ADIs, including non-SFI ADIs, to meet with respect to IRRBB.

In line with APRA’s approach to better regulation under MPA, APRA has removed duplication of risk management requirements between CPS 220 and APS 117. Certain requirements in APS 117 have been retained where necessary to reflect the specific nature of IRRBB management and risk management.

This approach clarifies and simplifies the list of risk management requirements for ADIs as they will only appear in one area of the prudential framework. In updating APS 117, APRA has not added or removed IRRBB management framework and governance requirements and has only focused on not replicating requirements in multiple areas in its prudential framework.

The amendments to APS 117 are visible through the version of APS 117 that has been marked-up from the draft consulted on in November 2022, which has been released alongside this response paper.

Chapter 3 - Requirements for non-SFIs

This chapter initiates APRA’s consultation on extending certain requirements of APS 117 to non-SFIs. It provides background on why APRA is consulting on these requirements and sets out the requirements.

3.1 Recent international events

The failure of three US regional banks in March 2023 highlighted that IRRBB poses risks to the financial soundness of a bank and the importance of adequate IRRBB risk management. These banks were below the USD 250 billion threshold to be considered systemically important in the US. Non-systemically important banks in the US are subject to less stringent regulatory and supervisory requirements, including requirements around IRRBB. These banks were not required to mark-to-market their liquid asset portfolio, which meant that as interest rates increased the market value loss on their fixed rate assets, measured at amortised cost, was not reflected in their capital position.

APRA’s prudential framework includes simplified capital requirements for small, less complex ADIs that are commensurate with the nature, scale and complexity of the ADI’s operations. Australian ADIs with total assets below $20 billion are eligible to use the simplified requirements and are categorised as non-SFIs (unless otherwise directed by APRA). These ADIs are generally locally incorporated, with no trading book activities, offshore businesses, or international funding sources.

Under APRA’s simplified framework, there are currently no explicit IRRBB requirements – APS 117 does not apply to non-SFIs. Instead, non-SFIs must follow the risk management requirements set out in CPS 220. Non-SFIs are also required to provide APRA with balance sheet repricing profile information under ARS 117.0.

3.2 The proposed requirements

APRA considers it appropriate to consult on extending certain IRRBB prudential requirements to non-SFIs to clarify that all ADIs are required to prudently manage their IRRBB, relative to the nature, scale and complexity of the ADI’s operations. The draft IRRBB requirements in APS 117 build on the general risk management requirements set out under CPS 220 and confirm that IRRBB is a material risk for the purposes of CPS 220.

APRA is also proposing that all ADIs (including non-SFIs) should ensure their Boards and senior management are aware of the ADI’s IRRBB exposure. APRA is also reiterating that where a non-SFI is not appropriately managing its IRRBB, APRA may require the non-SFI to comply with some or all requirements set out in APS 117 that apply to SFIs.

Given these requirements are an extension of APRA’s risk management requirements set out in CPS 220, APRA does not expect these requirements to materially increase the regulatory impact for non-SFIs. APRA expects prudent non-SFIs would already have in place appropriate IRRBB risk management practices that align with the requirements set out in APS 117.

The draft requirements that APRA is proposing to extend to non-SFIs, so that the requirements apply to all ADIs, are set out below. Following a three-month consultation period, APRA intends to formalise and embed these requirements in APS 117.

Draft new prudential requirements for all ADIs

14. IRRBB is a material risk and is a category of market and investment risk under Prudential Standard CPS 220 Risk Management (CPS 220). As part of its risk management framework required under CPS 220, an ADI must ensure that it appropriately manages its IRRBB, commensurate with the nature, scale and complexity of its operations.

15. An ADI’s senior management must regularly (at least semi-annually) report its IRRBB exposure to its Board or Board committee.

16. Where APRA determines that an ADI is not appropriately managing, measuring or monitoring its IRRBB or is carrying excessive interest rate risk, APRA may require the ADI to comply with all or specific requirements in this Prudential Standard and/or require the ADI to hold additional regulatory capital, commensurate with the IRRBB risk.

Chapter 4 - Consultation

Alongside this response paper, APRA is releasing a draft APG 117 and draft new prudential requirements for all ADIs (paragraphs 14, 15 and 16 of draft APS 117), for consultation. APRA is not opening consultation on other requirements in the draft APS 117.

APG 117 assists ADIs in complying with the requirements set out in APS 117 and sets out prudent practices in relation to the management and measurement of IRRBB. The draft APG 117 is interspliced with the requirements set out in APS 117 to support ADIs in interpreting the guidance.

The new draft prudential requirements that extend to non-SFIs, as discussed in Chapter 3, intend to support non-SFIs in meeting the general risk management requirements for IRRBB set out in CPS 220. Following a three-month consultation period, APRA intends to finalise APS 117 alongside the final APG 117 in 2024. The draft requirements that extend to non-SFIs will come into effect as part of the revised APS 117 in October 2025. APRA’s consultation on APS 117 is focused on the draft requirements that extend to non-SFIs.

4.1 Request for submissions

APRA invites written submissions on the draft APG 117 and proposed new requirements that extend to non-SFIs. Written submissions should be sent to ADIpolicy@apra.gov.au by 1 March 2024 and addressed to:

General Manager, Policy

Policy and Advice Division

Australian Prudential Regulation Authority

4.2 Important disclosure notice — publication of submissions

All information in submissions will be made available to the public on the APRA website, unless a respondent expressly requests that all or part of the submission is to remain in confidence. Automatically generated confidentiality statements in emails do not suffice for this purpose. Respondents who would like part of their submission to remain in confidence should provide this information marked as confidential in a separate attachment.

Submissions may be the subject of a request for access made under the Freedom of Information Act 1982 (FOIA). APRA will determine such requests, if any, in accordance with the provisions of the FOIA. Information in the submission about any APRA-regulated entity that is not in the public domain and that is identified as confidential will be protected by section 56 of the Australian Prudential Regulation Authority Act 1998 and will therefore be exempt from production under the FOIA.

Footnotes

1 During a period of low interest rates following the COVID-19 pandemic, these banks accumulated large holdings of long-term fixed rate assets without hedging the underlying interest rate risk. The market value of these assets materially declined following a period of increasing interest rates, prompting concerns over the solvency of the banks if these losses were ‘realised’ to fund outgoing deposits. These concerns resulted in large deposit outflows that were exacerbated by the nature of the customer base – uninsured deposits held by commercial customers concentrated in similar industries. For further information, refer to: Review of the Federal Reserve’s Supervision and Regulation of Silicon Valley Bank.

2 Refer to: APRA Corporate Plan 2023-24.