Information paper - ADIs: Transitioning to the Financial Accountability Regime

Executive summary

The Financial Accountability Regime (FAR) aims to improve accountability standards in entities regulated by the Australian Prudential Regulation Authority (APRA), drive reform in operating culture and reinforce the standards of conduct expected by the Australian community. The regime is jointly administered by APRA and the Australian Securities and Investments Commission (ASIC) (collectively, the Regulators).

The FAR replaces the Banking Executive Accountability Regime (BEAR) and will apply to authorised deposit-taking institutions (ADIs) and their authorised non-operating holding companies (NOHCs) from 15 March 2024.

ADIs must continue to comply with the BEAR in the period leading up to the FAR commencing. There is no gap in application of the two regimes.

The FAR is a strengthened and broadened accountability regime. The key differences from the BEAR are that the FAR:

- expands the regime to authorised NOHCs of ADIs;

- expands the regime to include superannuation and insurance entities and their licensed NOHCs;

- expands the regime to include a conduct focus;

- requires accountable entities to identify their significant related entities (SREs); and

- introduces the concept of ‘enhanced notification obligations’, where only enhanced entities must prepare and submit accountability statements and maps to the Regulators. As currently proposed under the draft Financial Accountability Regime Minister Rules 2022, ADIs subject to enhanced notification obligations include those with an asset size greater than $10 billion.

This information paper helps ADIs transition from the BEAR to the FAR. It includes the information they must provide to the Regulators.

In transitioning from the BEAR to the FAR, APRA Connect will be used for FAR data collection. For example, registrations, notifications, and lodgements of accountability maps and statements.

The FAR transitional arrangements ensure an ADI is not required to re-register those accountable persons already registered under the BEAR. However, the BEAR and FAR obligations are not identical. ADIs will need to check information previously submitted to APRA under the BEAR, and update that information as required.

Key activities for a large, complex (enhanced) ADI include:

- determining its entity profile;

- identifying which of its subsidiaries will become SREs;

- allocating additional prescribed responsibilities to existing or new accountable persons;

- allocating all applicable key functions to the relevant accountable persons;

- updating/preparing the accountability statements of existing or new accountable persons; and

- updating its accountability map.

Key activities for a small, simple (core) ADI with no subsidiaries include:

- determining its entity profile;

- allocating additional prescribed responsibilities to existing or new accountable persons;

- allocating all applicable key functions to the relevant accountable persons; and

- updating its internal accountability documentation.

In preparation for the commencement of the FAR, the Regulators will:

- host ADI and industry briefings from October 2023; and

- expect ADIs to participate in pre-commencement activities from October 2023 to make the transition as smooth as possible.

1 Overview

1.1 Purpose of this information paper

This information paper helps ADIs transition from the BEAR to the FAR. It includes the information they must provide to the Regulators.

Note: In this information paper, a reference to ADIs generally includes a reference to ADIs and their authorised NOHCs unless the context suggests otherwise.

This information paper should be read in conjunction with:

- the Financial Accountability Regime Act 2023 (FAR Act) and the Financial Accountability Regime (Consequential Amendments) Act 2023 (FCA Act);

the Joint Administration Agreement (JAA), which is an agreement between the Regulators that sets out the arrangements for joint administration of the FAR;

Note: The JAA was established under s37(1) of the FAR Act.

- the explanatory memorandum that accompanied the Financial Accountability Regime Bill 2023 and Financial Accountability Regime (Consequential Amendments) Bill 2023 (Explanatory Memorandum);

the draft Financial Accountability Regime Minister Rules 2022 (Minister rules);

Note: As at the issue of this information paper, the Minister rules are yet to be finalised. The details set out in this information paper in relation to enhanced obligation thresholds, prescribed responsibilities and positions, and references to the Minister rules are based on the exposure draft released by the Commonwealth Treasury on 12 September 2022.

the draft Financial Accountability Regime Act (Information for register) Regulator Rules 2023 (Regulator rules), which prescribe specific data items for inclusion in the FAR register (established under s40 of the FAR Act); and

Note: Regulator rules are legislative instruments and when made appear on the Federal Register of Legislation.

- the draft Financial Accountability Regime (Consequential Amendments) Transitional Rules 2023, which prescribe specific data items to be provided by ADIs for their existing BEAR accountable persons during transition to the FAR.

1.2 Summary of what ADIs need to do to transition

To transition from the BEAR to the FAR, ADIs will need to:

determine whether they are an ‘enhanced’ or ‘core’ entity—see section 1.3;

Note: The thresholds for determining whether an ADI is an enhanced or core entity are set out in Part 3 of the Minister rules.

- provide additional information for the FAR register and for those accountable persons transitioning from the BEAR to the FAR—see section 3.1;

- apply for registration for any new accountable persons (including for their SREs)—see section 3.2;

- for enhanced entities, update their accountability map and statements to reflect the expanded scope of the FAR—see Chapter 4;

- put in place processes and procedures to ensure they comply with their notification obligations—see Chapter 5;

- for entities that are part of a corporate group, determine the impact of the FAR on other entities within its group (including any SREs)—see Chapter 6; and

- maintain compliance with BEAR deferred remuneration obligations for six months after the commencement of the FAR, as well as comply with other transitional arrangements—see Chapter 7.

1.3 Overview of the FAR

The Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry (Royal Commission) recommended that provisions modelled on the BEAR be extended to all APRA-regulated entities, including APRA-regulated insurers and registrable superannuation entity (RSE) licensees. The Royal Commission also recommended the extended regime be jointly administered by the Regulators, with APRA overseeing prudential aspects and ASIC overseeing matters that concern consumer protection and market conduct.

Some obligations will vary, based on whether the ADI is classified as a core entity or an enhanced entity.

The FAR introduces the concept of ‘enhanced notification obligations’. Under these obligations, only enhanced entities are required to prepare and submit accountability statements and maps to the Regulators. The thresholds for determining whether an ADI is core or enhanced is based on asset size or the classification of other accountable entities within the same corporate group. ADIs will need to determine whether they are core or enhanced entities.

Note: As proposed in the draft Minister rules, an enhanced ADI will include those with an asset size greater than $10 billion.

Appendix A summarises the main differences between the BEAR and the FAR.

1.4 Key dates for ADIs and FAR commencement

Table 1 sets out the key dates for FAR commencement.

Table 1: Key dates for FAR commencement

Date | Event |

|---|---|

14 September 2023 | FAR Act received Royal Assent. Between this date and commencement of the FAR, ADIs are expected to participate in pre-commencement activities to make the transition as smooth as possible: see section 2.2. |

15 March 2024 | FAR commences for ADIs. BEAR deferred remuneration obligations continue to apply. |

15 September 2024 | FAR deferred remuneration obligations apply to ADIs. BEAR deferred remuneration obligations cease to apply to ADIs. |

2 Joint administration and pre-commencement

This chapter sets out:

- the Regulators’ approach to joint administration of the FAR (see section 2.1); and

- the pre-commencement arrangements for ADIs (see section 2.2).

2.1 The Regulators’ approach to joint administration

APRA and ASIC each have responsibility for the general administration of FAR. However, ASIC can perform certain functions and exercise certain powers only in relation to:

- ADIs that hold an Australian financial services licence or Australian credit licence;

- the SREs of such ADIs; and

- accountable persons of such ADIs and their SREs.

Such ADIs are referred to as dual-regulated ADIs.

The Regulators published the JAA in October 2023. The JAA outlines the Regulators’ approach to joint administration.

The Regulators are collaborating to ensure they administer the FAR in an efficient and consistent way. Close engagement between the Regulators will minimise duplication of effort and facilitate streamlined and efficient engagement with ADIs.

2.1.1 Single point of contact

The Regulators have established a single point of contact (SPOC) for ADIs to raise queries or requests. The SPOC email address is FAR@apra.gov.au.

All queries or requests submitted through the SPOC email address will be triaged and allocated within APRA or ASIC as appropriate. Additionally, ADIs can apply for relief under relevant provisions of the FAR Act by writing to this email address.

Note: The Regulators have powers to adjust the operations of certain provisions of the FAR Act for specific accountable entities.

ADIs can still contact either regulator directly as required.

2.1.2 Single portal

APRA Connect will be used for the FAR data collection—for example, registrations, notifications, and lodgements of accountability maps and statements. ADIs do not need to submit the same information to each regulator separately. Information submitted by dual-regulated ADIs through APRA Connect will be made available to both APRA and ASIC for review.

2.2 Pre-commencement arrangements for ADIs

2.2.1 ADI submission of draft FAR information

ADIs will follow a two-step process to prepare for the FAR commencement. ADIs will submit draft submissions during the pre-commencement period, which the Regulators will review and give feedback on. ADIs will then make a formal submission, based on that feedback.

Starting from November, ADIs will provide the following information, via APRA Connect:

- entity profile information, including whether the ADI is classified as an enhanced or core entity, whether it is sole or dual-regulated, and its nominated SREs;

- draft additional information for existing accountable persons under the BEAR to be included in the FAR register;

- draft registration information for any new accountable persons; and

- for enhanced entities, their updated draft accountability statements and map.

The detailed process and timelines for submitting information to the Regulators during the pre-commencement period and for formal submission will be released when the Regulators finalise the Regulator rules and Transitional rules.

2.2.2 Pre-commencement support arrangements for ADIs

The Regulators will host ADI and industry briefings from October 2023. Further details on these briefings will follow. The purpose of these briefings is to help ADIs prepare for the administrative and operational requirements of implementing the FAR.

3 Registration of accountable persons

This chapter sets out:

- the transition for accountable persons who are already registered under the BEAR and will be accountable persons under the FAR (see section 3.1);

- the process for new accountable person registrations (see section 3.2);

- the requirements for filling temporary and unforeseen vacancies (see section 3.3); and

- how to assign key functions to accountable persons (see section 3.4).

3.1 Transitioning accountable persons from the BEAR to the FAR

The FAR transitional arrangements ensure an ADI is not required to re-register those accountable persons already registered under the BEAR: see item 4 of Sch 2 to the FCA Act.

However, as the BEAR and FAR obligations are not identical, ADIs will need to check information previously submitted to APRA under the BEAR, and update that information. Differences include:

- prescribed responsibilities—both new and existing (as prescribed under the Minister rules)—to reflect that obligations under the FAR cover both prudential matters and conduct-related matters;

- the new scope of entities in an ADI group that are subject to the FAR obligations—other entities in an ADI group may be accountable entities (including an authorised NOHC of an ADI) or SREs of the ADI; and

- additional information that ADIs must include in the FAR register, which was not required under the BEAR.

As a result of these differences, an ADI will have to consider whether new accountable persons need to be registered and whether the responsibilities of any of its accountable persons registered under the BEAR needs to be amended. It is critical this process is robust and comprehensive to ensure the responsibilities of an ADI’s accountable persons cover the operations of the ADI and its relevant group.

Note: The relevant group of an accountable entity is the accountable entity and its SREs—see s8 of the FAR Act.

In some cases the ADI and its relevant group will form part of a larger corporate group that includes other APRA-regulated entities. When this occurs, ADIs will need to carry out this exercise holistically to ensure accountability is apportioned appropriately and in a manner that aligns with the governance arrangements of the group.

3.2 Application for registration of a new accountable person

ADIs can apply for registration of new accountable persons under the FAR from one month before the commencement of the FAR. ADIs are also able to apply for registration of new accountable persons under the BEAR during this time (i.e. there will be parallel processes). APRA will manage this parallel process as set out in Table 2.

Table 2: Parallel process for registration of new accountable persons

Application type | APRA action |

|---|---|

Effective date of appointment of the accountable person is on or before the day before the FAR commences | APRA will process the application as per existing procedures under the BEAR. |

Effective date of appointment of the accountable person is on or after the day the FAR commences, submitted within two weeks before FAR commencement | APRA will strongly encourage the ADI to submit the application under the FAR rather than under the BEAR. |

Pending applications for registration under the BEAR | These applications will automatically transfer as a new registration application under the FAR on the day the FAR commences. APRA will take these pending applications to be applications submitted on the FAR commencement date and will have a registration period of 21 days assigned from that date and the processes for FAR applications will apply. |

Note: For more information on pending applications to register a person under the BEAR, see item 6 of Sch 2 to the FCA Act.

3.3 Filling temporary and unforeseen vacancies

Under the BEAR, there may be persons who are not registered as accountable persons because they are performing their role in response to a temporary or unforeseen vacancy. Individuals acting in this way when the FAR obligations commence for ADIs will transition across to the FAR on the same basis, and are able to continue filling temporary or unforeseen vacancies without registration for a further 90 days: see item 7 of Sch 2 to the FCA Act.

3.4 Concept and application of key functions

The Regulators have recently consulted on the proposed Regulator Rules, Transitional Rules and ADI key functions descriptions and have received submissions in response to that consultation. The Regulators are currently considering the matters raised in those submissions and intend that relevant guidance will align with the final versions of the Regulator Rules, Transitional Rules and ADI key functions descriptions.

3.4.1 The concept of key functions

In implementing the BEAR, APRA provided guidance on typical key functions for ADIs to consider when developing accountability statements. This list of key functions was non exhaustive, but reflected areas an ADI was expected to consider carefully when refining and clarifying areas of accountability.

The term ‘key functions’ now has a different meaning under the FAR. Under the FAR:

- key functions are prescribed in the Regulator rules;

- each key function that is applicable to the ADI must be assigned to at least one accountable person and recorded in the FAR register; and

- changes to the allocation of key functions are considered material changes and must be reported under the FAR notification obligations (see section 5.1.1).

The concept of key functions does not expand the definition or scope of responsibilities of accountable persons under the Minister rules and s10 of the FAR Act. An applicable key function can only be allocated to an identified accountable person.

Table 3 sets out the key differences between prescribed responsibilities and positions set out in the Minister rules and the key functions set out in the Regulator rules.

Table 3: Key differences between prescribed responsibilities and positions and key functions

Feature | Prescribed responsibilities and positions | Key functions |

|---|---|---|

Authority | Defined under s10(2) and (3) of the FAR Act and prescribed under the Minister rules. | Prescribed information for inclusion in the FAR register under the Regulator rules. |

Purpose | To identify accountable persons (i.e. an individual that holds one or more prescribed responsibilities and/or positions is an accountable person). | To assist the Regulators in assessing whether accountable entities are adequately assigning accountability across all operational areas to their accountable persons (i.e. key functions can only be assigned to identified accountable persons). |

Scope | End-to-end accountability (i.e. an individual that holds a prescribed responsibility or position has end-to-end accountability in relation to that prescribed responsibility or position). | The assignment of a key function to an accountable person does not necessarily mean that the accountable person has end-to-end accountability in relation to that key function (i.e. there may be different responsibilities around that key function). |

Joint accountability | Joint accountability applies where one or more individuals are holding the same prescribed responsibility or position: see s21(2) of the FAR Act. | Joint accountability does not necessarily apply where multiple accountable persons have been assigned the same key function, given those accountable persons do not necessarily have end-to-end accountability in relation to that key function. |

3.4.2 Application of key functions

Key functions do not create any new responsibilities for accountable persons. As part of their key personnel obligations under s23(1) or s23(3) of the FAR Act, ADIs are required to nominate their accountable persons to be responsible for every area of their business operations. Therefore, the need to allocate applicable key functions will not result in ADIs having to register lower-level executives as accountable persons.

However, the Regulators emphasise that given the list of ADI key functions outlined in the Regulator rules is non-exhaustive, the allocation of all applicable key functions would not, in itself, ensure compliance with the key personnel obligations.

ADIs must assess which of the key functions are applicable to them, which must then be allocated to the relevant accountable person(s). The Regulators acknowledge that some of the ADI key functions outlined in the Regulator rules may not be applicable to authorised NOHCs of an ADI or foreign ADIs.

Note: The key functions concept does not apply to SREs. ADIs are not required to consider if any of the ADI key functions are applicable to their SREs.

ADIs have discretion about which key functions are assigned to which accountable persons, as long as it reflects actual practices. One accountable person may have no key functions assigned to them, while another accountable person may have multiple key functions. ADIs can assign a key function to more than one accountable person if this reflects different responsibilities in relation to that function.

The assignment of a key function to an accountable person does not automatically mean that the accountable person has end-to-end accountability in relation to that key function: see Example 1.

Example 1: Assigning key functions to more than one accountable person

There may be several accountable persons assigned to an ADI’s credit risk management key function. For example, in one ADI:

- the chief executive officer is accountable for ensuring that the ADI as a whole operates within the board-approved credit risk appetite;

- the chief risk officer is accountable for the overall risk controls and overall risk management arrangements, and participates in material credit decisions;

- the head of retail banking is responsible for managing the credit risk generated by the retail banking division; and

- the head of business banking is responsible for managing the credit risk generated by the business banking division.

4 Enhanced ADIs: Accountability statements and maps

Enhanced ADIs need to prepare the following two documents that core entities do not:

accountability statements, for each accountable person, which contain a comprehensive statement of that person’s responsibilities; and

Note: Individuals that are accountable persons for multiple entities within a group, or are accountable for multiple responsibilities, need only submit one accountability statement.

- an accountability map, which outlines all accountable persons in the relevant group, their responsibilities, and the lines of reporting and responsibility between them.

This chapter sets out what enhanced ADIs need to include in their accountability statements and maps (see section 4.1) and how to submit and update their statements and maps (see section 4.2).

Core ADIs are not required to provide an accountability map or statements to the Regulators. However, all ADIs should continue to document their accountability arrangements, including how they comply with their key personnel obligations.

See Appendix A for a summary of the key differences between BEAR and FAR in relation to statements and maps and the expected effect on ADIs.

4.1 Content of accountability statements and maps

The Regulators have provided a template as a guide to the format and minimum content of accountability statements: see Financial Accountability Regime: ADI accountability statement guidance and template. This is broadly aligned with the template and guidance provided by APRA under the BEAR. The Regulators are taking a principles-based approach to administering obligations about the content of statements and maps, and will periodically assess whether additional content needs to be prescribed in the Regulator rules.

Individual statements must reflect actual accountability as it operates in practice within the ADI and its relevant group. Accountability statements should be specific to both the ADI and the individual accountable person.

For those accountable persons of enhanced ADIs who are transitioning from the BEAR to the FAR, accountability statements provided to APRA under the BEAR will automatically transition to be accountability statements under the FAR: see item 13 of Sch 2 to the FCA Act and paragraph 1.307 of the Explanatory Memorandum. Although such accountable persons do not need to be re-registered, an enhanced ADI’s accountability statements and map will need to be revised and resubmitted in light of:

- the application of the FAR to its SREs and any authorised NOHC of the ADI;

- new prescribed responsibilities that may either result in new accountable persons being registered or existing accountability statements being updated to reflect changes in the accountable person’s responsibilities;

- the FAR requirement for accountability statements to include a declaration by the accountable person that the statement is accurate and they understand their accountability obligations; and

- new accountability obligations of accountable persons to cover dealing with the Regulators and taking reasonable steps to prevent matters from arising that would likely result in the ADI materially contravening specified financial sector laws (see s21 of the FAR Act).

The Regulators expect the content of the accountability statement of an accountable person would align with the accountable person’s allocated key function(s), if any. However, the Regulators do not expect the allocation of any key function(s) to an accountable person would, in itself, materially reshape the content or structure of the accountability statement of the accountable person.

4.2 Process for submitting and updating statements and maps

ADIs must submit their updated accountability map and statements in PDF or Word format. In relation to draft accountability statements and maps submitted during the pre-commencement period, the Regulators expect that these documents will present the changes (from BEAR maps and statements) in mark-up. This will expedite the Regulators’ review process. When formally submitting an updated map and statements under the FAR, the Regulators request that marked-up changes be removed.

5 Notification obligations

All ADIs are required to meet the core notification obligations (see section 5.1), while only enhanced ADIs are subject to enhanced notification obligations (see section 5.2). The small, medium and large classifications that operated under the BEAR will no longer apply. Authorised NOHCs of ADIs will be subject to the same notification obligations as other accountable entities within their corporate group.

Another change from the BEAR is the introduction of two new events that must be notified to the Regulators: see s32(d)(i) and 32(e) of the FAR Act. These are when:

- the accountable entity has reasonable grounds to believe that it has breached its key personnel obligations (see section 5.1); and

- a material change occurs to information about an accountable person on the FAR register (see section 5.2).

ADIs must provide notice to the Regulators within 30 days of a notifiable event: see s31(6) of the FAR Act. The notice must be provided by creating, completing and submitting the relevant FAR notification return in APRA Connect.

Additionally, an ADI must take reasonable steps to ensure that each of its SREs complies with the notification obligations as if they were accountable entities: see s31(1)(b) of the FAR Act.

5.1 Core notification obligations

ADIs must notify the Regulators through APRA Connect when an accountable person of the ADI or of an SRE of the ADI:

- ceases to be an accountable person;

- is dismissed or suspended because the person has failed to comply with their accountability obligations (see s21 of the FAR Act); or

- has their variable remuneration reduced because the person has failed to comply with their accountability obligations.

The ADI must also notify the Regulators if:

- it has reasonable grounds to believe that:

- it has failed to comply with its accountability obligations (see s20 of the FAR Act) or its key personnel obligations (see s23 of the FAR Act); or

- an accountable person of the ADI, or of an SRE of the ADI, has failed to comply with their accountability obligations (see s21 of the FAR Act); and

- it has failed to comply with its accountability obligations (see s20 of the FAR Act) or its key personnel obligations (see s23 of the FAR Act); or

- a material change occurs to information that relates to an accountable person of the ADI, or of an SRE of the ADI, and is contained in the FAR register (see s32 of the FAR Act).

5.1.1 Material changes to information contained in the FAR register

A material change to the FAR register would include a change in the assignment of a key function to an accountable person. However, changes that are trivial in nature (such as the correction of an immaterial typographical error) would not be considered a material change.

5.2 Enhanced notification obligations

Enhanced ADIs must notify the Regulators through APRA Connect of material changes to their accountability statements and map.

Note: Additional information about the accountability map and statements, and the obligations to provide those documents, is set out in Chapter 4.

It is the responsibility of an ADI to determine whether a change is material in nature. The ADI must consider all of the relevant circumstances and, in turn, determine whether one or more of the notification requirements has been triggered. A change is likely to be material if a reasonable person, taking into account all knowledge of all relevant facts and circumstances, would conclude that the change is material.

5.2.1 Material changes to accountability statements and maps

A change to an accountability statement or map is likely to be material if the accountability statement or map no longer accurately reflects the operations of the ADI and its SREs, or the responsibilities and reporting lines of each accountable person.

Examples of changes that are likely to be considered material include changes to:

- the substance of an accountability or operations, such that an ADI is doing something additional, or not doing something it did previously;

- prescribed responsibilities or positions of an accountable person;

- general responsibilities or underlying accountabilities of an accountable person, such as where accountability is altered from ‘ensure’ to ‘oversight’; or

- who the accountable person reports to (see s31(2)(b) and (d) of the FAR Act).

In preparing for the FAR, ADIs may adjust their accountability frameworks. These adjustments may result in material changes to their existing accountability statements and maps. These adjustments could include:

- incorporating their authorised NOHCs and SREs;

- adding mandatory declarations within statements for existing accountable persons in accordance with the requirement for accountability statements under the FAR;

- assigning key functions to accountable persons; or

- reflecting a new prescribed responsibility and/or position, particularly the new conduct responsibilities, which causes a person to be an accountable person under the FAR.

In contrast, changes to an accountability statement or map that are unlikely to be considered material include changes to:

- the title of a person who reports to an accountable person, where there is no substantive change to the reporting line or the line of responsibility of that accountable person;

- the name of a business unit within the ADI where the underlying accountabilities or operations of and responsibility for the unit remain the same; or

- references to relevant legislation or Regulator rules that do not alter the accountabilities or responsibilities of an accountable person.

While these sorts of changes are unlikely to be considered material, they should nonetheless still be incorporated into the revised accountability statements and map (as applicable). ADIs must submit the accountability statements and maps with any notifications regarding a material change.

6 Corporate groups

The FAR applies to an ADI (including an authorised NOHC of the ADI) directly and to their SREs indirectly. ADIs must take reasonable steps to ensure their SREs comply with certain FAR obligations as if those SREs were also accountable entities.

This chapter sets out:

- how to identify SREs of an ADI (see section 6.1);

- the classification of accountable entities within corporate groups (see section 6.3); and

- how to prepare accountability statements and maps for individuals who are accountable persons for multiple entities within the same corporate group (see section 6.4).

There are two key differences between how the BEAR and the FAR apply to the corporate group of an ADI. These differences are:

- the scope of a relevant group; and

- the classification of an ADI within a corporate group with multiple accountable entities, including across other relevant industries, for the purpose of determining its notification obligations.

See Appendix A for a summary of the key differences between the regimes from an ADI group perspective.

6.1 Identifying SREs of an ADI

All ADIs, including foreign ADIs, and their authorised NOHCs will need to identify all of their SREs. An entity is an SRE of an ADI if, among other things:

- it is a subsidiary of the ADI;

- it is not an accountable entity itself; and

its business or activities have or are likely to have a material and substantial effect on the ADI.

Note: See s12 of the FAR Act for definition of ‘significant related entity’ and s12(2) for certain exceptions.

Factors that an ADI can consider when assessing whether a subsidiary is an SRE include:

- the nature and scale of the subsidiary’s business or activities;

- the nature and extent of any interdependency between the subsidiary and the ADI; and

- any organisational, financial or administrative arrangements between the subsidiary and the ADI (see s12(4) of the FAR Act).

A subsidiary could have a material and substantial effect on an ADI if the subsidiary’s business activity has the potential, if disrupted, to have a significant impact on the business operations of the ADI or its relevant group, or their ability to manage risks effectively: see paragraph 1.36 of the Explanatory Memorandum. This is similar to the definition of ‘material business activity’ in APRA’s prudential standards on outsourcing.

Note: Prudential Standard CPS 231 Outsourcing, Prudential Standard HPS 231 Outsourcing and Prudential Standard SPS 231 Outsourcing all include similar definitions of ‘material business activity’.

The Regulators expect an ADI to put in place robust processes and procedures to assess which of their subsidiaries are SREs. Such processes and procedures should align and integrate with the ADI’s broader risk management framework.

The Regulators may query or request information regarding an ADI’s assessment processes and outcomes.

6.2 Foreign accountable entities

A foreign ADI (as defined in the Banking Act 1959) is a foreign accountable entity under the FAR. As such, only the branch operations of the foreign ADI within Australia will be subject to the obligations under the FAR: see s(8) and s15(2)(b) of the FAR Act. The FAR requires a foreign accountable entity to ensure that the responsibilities of the accountable entity’s accountable persons cover all parts or aspects of the operations of each branch of the accountable entity operating in Australia: see s23(3)(a) of the FAR Act.

In addition, a foreign ADI must identify whether it has any SREs. In doing so, the foreign ADI has to consider whether a subsidiary could have a material and substantial effect on its Australian branch operations rather than the foreign ADI as a whole.

6.3 Classification of accountable entities within groups

If one accountable entity in a corporate group is classified as an enhanced entity, then all other accountable entities within that corporate group will also be classified as enhanced entities: see s33 of the Minister rules.

6.3.1 Corporate groups with accountable entities from other relevant industries

When the FAR commences for insurers, authorised and registered NOHCs of insurers, and RSE licensees, the classification of existing accountable entities in a corporate group that includes any such entities may change. For example, an ADI and an authorised NOHC of an ADI may become enhanced entities for the purposes of complying with relevant notification obligations under the FAR: see Example 2.

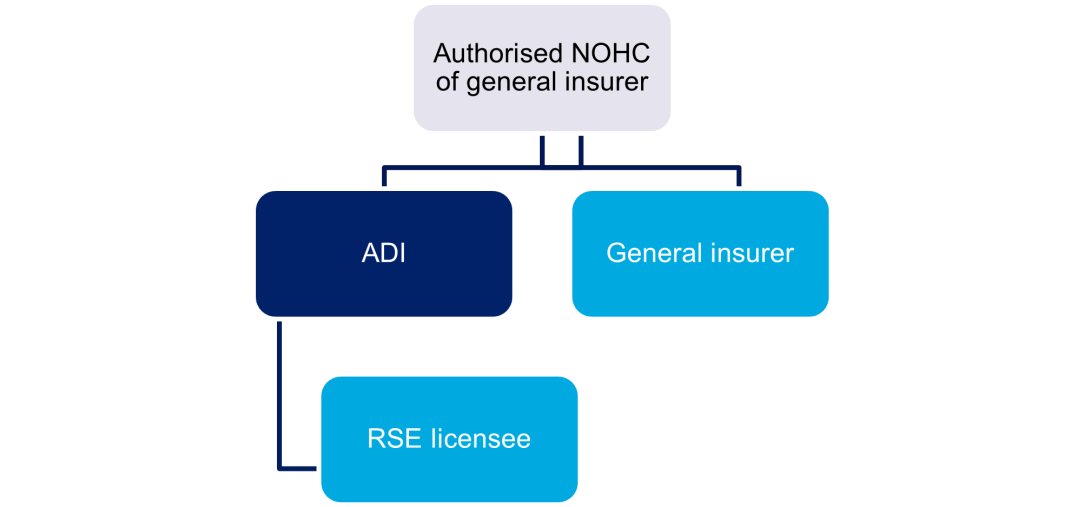

Example 2: An ADI that is part of a corporate group that will include other accountable entities

In Figure 1, an ADI is part of a corporate group that includes a number of other entities that will become accountable entities. The ADI does not meet the enhanced notification threshold; however the general insurer will meet that relevant threshold when the FAR commences for that entity. Before the FAR commences for insurers, authorised and registered NOHCs of insurers, and RSE licensees, the RSE licensee (which is a subsidiary of the ADI) is, in this example, an SRE of the ADI.

Figure 1: Example structure

When the FAR commences for insurers, authorised and registered NOHCs of insurers, and RSE licensees:

- the ADI will be reclassified from core to enhanced. This is because the general insurer meets the relevant enhanced notification threshold and, therefore, all accountable entities within the same corporate group will also be classified as enhanced for this purpose; and

- the RSE licensee will cease to be an SRE when it becomes an accountable entity. This will likely trigger a number of obligations under the FAR. For example, the ADI will likely need to make material changes to its accountability statement(s) and map. In addition, the ADI may need to notify the Regulators of the cessation of an accountable person of an SRE of the ADI, as that person will instead become an accountable person of the RSE licensee in its capacity as an accountable entity. The RSE licensee will also be classified as an enhanced entity because it is within a corporate group that includes an enhanced entity.

When an insurer or RSE licensee ceases to be an SRE of an ADI (i.e. because it becomes an accountable entity), the ADI will need to consider the consequences of the change under the FAR.

6.4 Accountability statements and maps

An individual may be an accountable person of multiple accountable entities and/or SREs within the same corporate group. As with the BEAR, if the enhanced notification obligations under the FAR apply, those entities may choose to prepare and submit one single accountability statement covering all relevant matters for that individual. However, the individual’s allocated areas of accountability and responsibility for each accountable entity and SRE must be able to be clearly identified.

Similarly, where there are multiple accountable entities within the same corporate group and the enhanced notification obligations under the FAR apply, it is open to those entities to prepare and submit one single accountability map covering all relevant accountable persons. However, the details of the reporting lines and lines of responsibility of all accountable persons of each accountable entity and SRE must be able to be clearly identified.

7 Deferred remuneration obligations and other transitional matters

This chapter sets out how, during the transition period, ADIs can comply with:

- the deferred remuneration obligations (see section 7.1);

- the notification obligations (see section 7.2); and

- other obligations that continue under the BEAR after FAR commencement (see section 7.3).

This chapter also sets out how regulatory actions under the BEAR will operate after FAR commencement: see section 7.4.

7.1 Deferred remuneration obligations

Deferred remuneration obligations refer to the obligation to defer a prescribed portion of the variable remuneration of an accountable person to ensure compliance with their obligations: see Pt 5 of Ch 2 of the FAR Act.

The FAR deferred remuneration obligations will apply to remuneration decisions that occur in the first financial year that begins six months after the FAR commences.

Prior to this time, the BEAR deferred remuneration obligations will still apply. Deferred remuneration will continue to be subject to the BEAR obligations until the period of deferral finishes.

Appendix A sets out the deferred remuneration obligations under the FAR compared to those under the BEAR.

7.1.1 Transition to the deferred remuneration obligations under the FAR

In transitioning to the FAR, ADIs will need to ensure they meet the deferral requirements under Prudential Standard CPS 511 Remuneration. These requirements come into effect on 1 January 2023 for ADIs that are significant financial institutions (SFIs) and 1 January 2024 for ADIs that are not SFIs (non-SFI ADIs).

Note: An ADI is an SFI when its total assets are in excess of $20 billion, or it is determined as such by APRA (taking into account matters such as complexity in its operations or remuneration practices, or its membership of a group).

For SFIs, the CPS 511 deferral requirements are typically more stringent than the deferred remuneration obligations under the FAR. Therefore, the CPS 511 deferral requirements would, in most cases, result in compliance with the FAR deferred remuneration obligations.

CPS 511 does not impose deferral requirements on non-SFI ADIs. These ADIs will, however, already be subject to BEAR deferred remuneration obligations. When non-SFI ADIs move to the FAR the option to defer a portion of total remuneration will be removed—the non-SFI ADI will be obliged to defer 40% of variable remuneration. Where relevant, a non-SFI ADI will need to update its remuneration plans and framework to reflect this shift.

Note: Under CPS 511, a foreign ADI with total assets in excess of $20 billion must defer the variable remuneration of its highly paid (i.e. total fixed remuneration plus actual variable remuneration that is equal to or greater than $1 million) material risk-takers.

Appendix B summarises the alignment in deferral requirements between CPS 511 and the FAR.

7.2 Notification obligations

7.2.1 Notification events

A BEAR notification event may occur in the month before the FAR commences. If this happens, the ADI must notify APRA of the event, even though the notification period will end after the FAR commences: see item 14 of Sch 2 to the FCA Act. The ADI should submit a notification form in accordance with the existing procedures under the BEAR.

7.2.2 Changes to accountability statements and maps under the BEAR

A change may arise in an accountability statement of an accountable person or the accountability map of an ADI in the month before the FAR obligations commence. If this happens, the ADI must notify APRA of any such change and submit a revised accountability statement or map. This is the case even if the 30-day notification period under the BEAR ends after the commencement of FAR and the ADI is not an enhanced entity under the FAR.

The ADI should submit the notification form together with the revised accountability statement or map in accordance with the existing procedures under the BEAR: see item 14 of Sch 2 to the FCA Act.

7.3 Other obligations that continue under the BEAR after FAR commencement

Certain other obligations under the BEAR will continue to apply after the commencement of the FAR to enable the effective transition from the BEAR: see paragraph 1.314 of the Explanatory Memorandum. This includes:

- following directions, either to reallocate responsibilities or for non-compliance; and

- enforceable undertakings and injunctions.

7.4 Regulatory actions under the BEAR after FAR commencement

APRA will continue to be able to exercise its powers under the BEAR after the FAR commences. Any decisions made under the BEAR can continue to be reviewed following the existing review procedures. Any action in progress under the BEAR by APRA may still proceed after the BEAR is repealed, including if the action relates to incidents that come to light after the FAR has commenced but relate to the period before the FAR commences.

The FAR can be used to take action in relation to breaches of the BEAR. Such action includes issuing a non-compliance direction and disqualifying an accountable person. Furthermore, if an accountable person is disqualified under the BEAR, they will continue to be disqualified under the FAR. An ADI can also have its authority revoked as a result of breaches of the BEAR, regardless of whether the breach was before or after the FAR commenced. Such breaches can be prosecuted under the FAR despite the breach occurring under the BEAR: see paragraph 1.320 of the Explanatory Memorandum.

Information collected under the BEAR can be used to investigate breaches under the FAR. This is regardless of whether the breach occurred before or after the FAR commences: see paragraph 1.321 of the Explanatory Memorandum.

Glossary

accountability map | A document that complies with s37FB of the BEAR or s34 of the FAR Act (as applicable) |

|---|---|

| accountability statement | A statement that complies with s37FA of the BEAR or s33 of the FAR Act (as applicable) |

| accountable entity | Accountable entity has the same meaning as set out in s9 of the FAR Act |

| accountable person | Accountable person has the same meaning as set out in s37BA and 37BB of Pt IIAA of the Banking Act 1959 or s10 and 11 of the FAR Act (as applicable) Note: See also Part 2 of the draft Minister rules. |

| ADI | Authorised deposit-taking institution |

| APRA | Australian Prudential Regulation Authority |

| ASIC | Australian Securities and Investments Commission |

| BEAR | The Banking Executive Accountability Regime, which is set out in Pt IIAA of the Banking Act 1959 (as in force up to and immediately before the commencement of Pt 2 of Sch 1 to the FCA Act) |

| core ADI | ADIs that are subject to only the core notification obligations set out in s31(1) of the FAR Act |

| CPS 511 | Prudential Standard CPS 511 Remuneration |

| dual-regulated ADI | An ADI that holds an Australian financial services licence or Australian credit licence, and is consequently regulated by APRA and ASIC |

| enhanced ADI | An ADI that is subject to both core and enhanced notification obligations under s31(1) and 31(2) of the FAR Act |

| enhanced notification thresholds | The thresholds that determine whether ADIs will need to meet the enhanced notification obligations in s31(2) of the FAR Act. The obligations apply if the ADI:

Note 1: There is no specific enhanced notification threshold set for NOHCs. Therefore, if an NOHC is part of a group that has an enhanced entity, that NOHC will be taken to have met the enhanced notification threshold itself and be subject to the enhanced notification obligations. Note 2: See s13–16 and 33 of the Minister rules for the full definition. |

| Explanatory Memorandum | The explanatory memorandum that accompanies the Financial Accountability Regime Bill 2023 and Financial Accountability Regime (Consequential Amendments) Bill 2023 |

| FAR | The Financial Accountability Regime established by the FAR Act and Sch 1 and 2 to the FCA Act (as the context requires) |

| FAR Act | Financial Accountability Regime Act 2023 (as may be amended or replaced from time to time) |

| FAR register | Register of accountable persons, established under and kept in accordance with s40 of the FAR Act |

| FCA Act | Financial Accountability Regime (Consequential Amendments) Act 2023 (as may be amended or replaced from time to time) |

| JAA | Joint Administration Agreement—an agreement between APRA and ASIC that sets out the arrangements for joint administration of the FAR (as may be amended or replaced from time to time) |

| key functions | Specified areas of responsibility that ADIs and authorised NOHCs of ADIs (as relevant) that are accountable entities must allocate to accountable persons, where applicable. Key functions provide a focus point for the Regulators to understand where accountability for matters of regulatory focus may sit within the accountable entity |

| Minister rules | Draft Financial Accountability Regime Minister Rules 2022 |

| NOHC | Non-operating holding company |

| pre-commencement period | The pre-commencement period for ADIs and authorised NOHCs of ADIs is the period between the commencement of the FAR Act and the date an ADI or an authorised NOHC of an ADI must start complying with FAR obligations (i.e. six months after the commencement of the FAR Act) |

| pre-commencement activities | Activities that ADIs and authorised NOHCs of ADIs are expected to engage in to facilitate:

|

| prescribed responsibilities and positions | Responsibilities and positions prescribed under the Minister rules that, if a person holds one or more, makes that person an accountable person Note: See s10(2)–(4) of the FAR Act for the full definition. |

| primary areas of focus | A non-exhaustive list of areas of accountability developed by the Regulators for enhanced entities to consider when developing their accountability statements |

| Regulator rules | Draft Financial Accountability Regime Act (Information for register) Regulator Rules 2023 (as amended or replaced from time to time) |

| Regulators | APRA and ASIC or either one of them, as the context requires |

| relevant group | The relevant group of an accountable entity means the accountable entity and its SREs: see s8 of the FAR Act |

| RSE licensee | Registrable superannuation entity licensee |

| SFI | An ADI or an authorised NOHC of an ADI which is a “significant financial institution”, being an ADI or authorised NOHC of an ADI that is:

Note: See Prudential Standard APS 001 Definitions. |

| SPOC | Single point of contact |

| SRE | Significant related entity—Has the meaning given in s12 of the FAR Act |

Appendix A: Key differences between the BEAR and the FAR requirements

Feature | BEAR | FAR | Expected effect on ADIs |

|---|---|---|---|

| Definition of accountable persons | An accountable person is defined by reference to a list of roles and responsibilities prescribed in the legislation and the general principle. | A longer list of roles and responsibilities prescribed in the Minister rules for the purpose of defining an accountable person and a general definition. | ADIs may identify additional accountable persons. ADIs will need to consider and allocate the extended list of prescribed responsibilities and positions to an accountable person and may need to revise their accountability maps and statements accordingly. |

| Accountability obligations—accountable entities | ADIs must take reasonable steps to comply with specified obligations that cover the way an ADI should conduct itself and how it should engage with APRA. While the BEAR does not impose direct obligations on subsidiaries of ADIs, ADIs are required to take ‘reasonable steps’ to ensure that their non-ADI subsidiaries comply with certain BEAR obligations. | In addition to the BEAR requirements, the FAR places obligations on ADIs to deal with both APRA and ASIC in an ‘open, constructive and cooperative way’. Under the FAR, accountable entities must take ‘reasonable steps’ to ensure that their SREs comply with certain FAR obligations. | Dual-regulated ADIs will need to engage with both APRA and ASIC on FAR matters. ADIs need to assess whether any of their related entities meet the criteria to become their SREs. |

| Accountability obligations—accountable persons | Accountable persons must comply with specified obligations. | In addition to the BEAR specified obligations, the FAR requires accountable persons to deal with both APRA and ASIC in an ‘open, constructive and cooperative way’. The FAR also requires accountable persons to take reasonable steps in conducting their responsibilities to prevent matters from arising that would (or would be likely to) result in the ADI’s material contravention of specified laws. | As with accountable entities, accountable persons will be required to deal with both APRA and ASIC on FAR matters. Additionally, the new obligation about contravening specific laws means the accountable person and ADI will need to consider what steps they must take to ensure compliance by the accountable person. |

| Deferred remuneration obligations | ADIs must defer the lesser of:

The specified percentage to be deferred varies based on the size of the ADI. | ADIs must defer 40% of the variable remuneration of all their accountable persons for a minimum of four years if the amount that would be deferred is greater than $50,000. All ADIs must comply with these deferred remuneration obligations, regardless of the size of the ADI. These obligations do not apply to those persons filling temporary or unforeseen vacancies of an accountable person under s24(2) and s30 of the FAR Act. | Deferred remuneration obligations for ADIs come into effect six months after the FAR commencement date for ADIs. Before that time, the BEAR deferred remuneration obligations continue to apply. Key definitions relating to remuneration are aligned with those in CPS 511. Appendix B provides more detail on the alignment between CPS 511 and the FAR deferred remuneration obligations. |

| Entity classification | Large, medium and small ADIs (relevant to commencement, remuneration and maximum civil penalties). | Accountable entities are subject to core notification obligations, or both enhanced and core notification obligations, based on thresholds set out in the Minister rules. | ADIs will need to determine the relevant notification obligations applicable to them. |

| General principle and particular or prescribed responsibilities | The general principle under s37BA(1) of the Banking Act 1959. Ten particular responsibilities under s37BA(3) of the Banking Act 1959. | The underlying concept of the general principle is retained but the specific term ‘general principle’ is no longer used. | ADIs will need to amend internal procedures for the new Minister rules. |

| Accountability maps and statements | All ADIs are required to submit accountability maps and statements. Statements are mandatory and comprehensive, with optional declaration. The content reflects obligations under the BEAR. Maps cover responsibilities and reporting lines of and between all accountable persons of an ADI and its subsidiaries. Content must reflect obligations under the BEAR. | Only enhanced entities must submit accountability maps and statements to the Regulators. The content of statements and maps have been expanded, in line with the obligations under the FAR. The declaration within accountability statements is mandatory. | Core entities are not required to submit an accountability map or statements, but they must identify and register accountable persons to cover all parts of their business, including each of the prescribed responsibilities and positions prescribed in the rules made by the Minister: see Chapter 4. Enhanced entities must review and revise statements and maps for their accountable persons to ensure new obligations are captured. |

| Changes to accountability maps and statements | ADIs must notify APRA of all changes to accountability maps and statements within 30 days of the change occurring. All ADIs must take reasonable steps to ensure that their non-ADI subsidiaries provide accountability statements to APRA and update APRA of any changes as if they were ADIs. | An enhanced entity must notify the Regulators of any material change to the accountability map and accountability statement(s) within 30 days of the change occurring. Enhanced entities must take reasonable steps to ensure their SREs provide accountability statements to the Regulators and update the Regulators of material changes as if they were accountable entities. | ADIs that are enhanced entities will need to implement new notification triggers. For guidance on what constitutes a material change: see section 5.2. |

| Notification obligations | ADIs must notify APRA when they become aware that they or their accountable persons have breached their accountability obligations. Additionally, ADIs must notify APRA if an accountable person is dismissed or suspended, or has their variable remuneration reduced, as result of breaching their accountability obligations. | All ADIs must provide the Regulators with certain information about the entity and its accountable persons. This includes notifying the Regulators when they have reasonable grounds to believe that:

Additionally, ADIs must notify the Regulators if an accountable person is dismissed or suspended, or has their variable remuneration reduced, as result of breaching their accountability obligations. | It is a new obligation to notify APRA and/or ASIC when the ADI has reasonable grounds to believe that it has breached its key personnel obligations. |

| Registration—temporary or unforeseen vacancies or other exceptions | If a person becomes an accountable person by filling a temporary or unforeseen vacancy, the ADI has 28 days to register the individual. | ADIs will have up to 90 days to register accountable persons filling temporary or unforeseen vacancies. No deferral of variable remuneration is required for any such accountable persons. Additionally, ADIs will have up to 30 days after the occurrence of the following events to register their relevant accountable persons:

| Temporary or unforeseen vacancies can now be filled for a longer period of time before the requirement to register an accountable person applies. This creates a simplified approach for temporarily filling vacancies, given there is no requirement to defer variable remuneration. |

| Application to groups | The BEAR applies to an ADI and its non-ADI subsidiaries, which are classified as large, medium or small based on its total assets. | The FAR applies to an ADI, an authorised NOHC of an ADI and their SREs. The ADI is classified as a core or enhanced entity, based on its total asset size, for the purpose of making relevant notifications. An authorised NOHC of an ADI will be determined solely by the classification of other accountable entities within the corporate group. However, where one of the accountable entities within a corporate group is classified as an enhanced entity, all accountable entities within that corporate group will be classified as enhanced entities, irrespective of the size of their total assets. | ADIs will have to assess whether any of their non-ADI subsidiaries are SREs and be aware of the classification of other accountable entities, if any, within their group. |

| Civil penalties and disqualification | Penalties are tiered based on the size of the ADI. The maximum penalty for:

APRA has a disqualification power to remove an individual from their role. A person could also be liable to a civil penalty for ancillary contravention of a BEAR obligation: see cl 3 of Sch 2 to the Banking Act 1959. | The maximum penalties under the FAR will be the greater of:

The Regulators have the power to disqualify a person from being an accountable person for a period. A person could also be liable to a civil penalty for ancillary contravention of a FAR obligation. | Larger maximum penalties will apply under the FAR. |

Appendix B: Alignment between FAR and CPS 511 deferred remuneration obligations

Feature | FAR | CPS 511 | Comparison |

|---|---|---|---|

| Scope | Entities: Applies to all ADIs. Persons: Accountable persons (directors and senior executives) Threshold: Defer if more than $50,000 in deferred variable remuneration | Entities: Applies to all ADIs. SFIs are subject to heightened deferral requirements; non-SFI ADIs do not have specific deferral requirements. Foreign ADIs with total assets in excess of $20 billion must defer the variable remuneration of their highly paid material risk-takers. Persons: Chief executive officers, senior managers, executive directors of SFIs, and highly paid material risk-takers (a material risk taker whose total fixed remuneration plus actual variable remuneration is greater than or equal to $1 million) of SFIs and foreign ADIs Threshold: Defer if $50,000 or more in deferred variable remuneration | The FAR variable remuneration deferral obligations set minimum standards and thus apply to ADIs regardless of size. The CPS 511 deferral requirements are more stringent than the FAR for SFIs and large foreign ADIs only. For non-SFI ADIs, only the FAR deferral obligations apply. |

| Meaning of ‘variable remuneration’ | Variable remuneration is the amount of a person’s total remuneration that is conditional on achievement of objectives: see s26(1)(a)(i) of the FAR Act. | Variable remuneration is the amount of a person’s total remuneration that is conditional on objectives, which include performance criteria, service requirements or the passage of time: see paragraph 18(w) of CPS 511. | The definitions are consistent; however, CPS 511 provides clarity to the term ‘objectives’. |

| Start of deferral period | The deferral period for variable remuneration starts at the beginning of the performance period (typically the beginning of a financial year). | The deferral period for variable remuneration starts at the beginning of the performance period (typically the beginning of a financial year). | Aligned. |

| Percentage of variable remuneration to defer | An accountable entity is required to defer 40% of the variable remuneration of all accountable persons for a minimum period of four years with no pro rata vesting permitted. | An SFI is required to defer for a:

Non-SFI ADIs have no specified deferral requirements. Foreign ADIs with total assets in excess of $20 billion must defer the variable remuneration of their highly paid material risk-takers. | There is a higher deferral threshold for chief executive officers under CPS 511. CPS 511 imposes more stringent requirements on SFIs, which are proportionate to the role of the individual. For non-SFI ADIs, the FAR minimums apply as CPS 511 does not impose deferral. |

| Value of deferred amount | The amount that must be deferred is based on the value of the variable remuneration as if it had been paid at the start of the performance period. | The amount that must be deferred is based on the value of variable remuneration awarded in the financial year: see Prudential Practice Guide CPG 511 Remuneration. | Aligned. Both regimes result in the same amount to be deferred, despite minor drafting variations. |

Disclaimer

APRA disclaimer and copyright

While APRA endeavours to ensure the quality of this publication, it does not accept any responsibility for the accuracy, completeness or currency of the material included in this publication and will not be liable for any loss or damage arising out of any use of, or reliance on, this publication.

© Australian Prudential Regulation Authority (APRA)

This work is licensed under the Creative Commons Attribution 3.0 Australia Licence (CCBY 3.0). This licence allows you to copy, distribute and adapt this work, provided you attribute the work and do not suggest that APRA endorses you or your work. To view a full copy of the terms of this licence, visit https://creativecommons.org/licenses/by/3.0/au/

ASIC disclaimer and copyright

This information paper does not constitute legal advice. We encourage you to seek your own professional advice to find out how the Corporations Act and other applicable laws apply to you, as it is your responsibility to determine your obligations.

Examples in this information paper are purely for illustration; they are not exhaustive and are not intended to impose or imply particular rules or requirements.

For ASIC purposes, this is Regulatory Guide 278 (RG 278).

© Australian Securities and Investments Commission