Financial Sustainability Challenges in Private Health Insurance

This letter sets out APRA’s expectations for private health insurers (PHIs) to improve their resilience to sustainability challenges. APRA signalled its focus on financial sustainability challenges in early 20181, calling out the risks posed by declining affordability for policyholders, and the impact on PHIs of government policy changes in response to cost pressure across the wider health system.

APRA recently completed an assessment of PHI resilience and their approaches to managing affordability and government policy change risks. APRA reviewed 15 PHIs chosen to provide a representative sample across the industry. Disappointingly, the review found many areas for improvement. This letter provides observations from the review and sets out APRA’s expectations for PHIs to improve resilience to these risks.

The review found PHIs had a strong awareness of these sustainability challenges. However, APRA’s assessment found many PHIs lacked credible strategies to mitigate the risks. APRA observed a concerning assumption made by many PHIs that Government would provide solutions. APRA believes that the complacent approach observed in the review is out of step with the significance of these risks to the industry.

APRA recognises the important role a stable and robust private health insurance industry plays to complement the universal public healthcare system in supporting the well-being of Australians. APRA’s role is to ensure the resilience of PHIs so they can continue to meet the promises made to policyholders and provide choice to consumers in managing their healthcare.

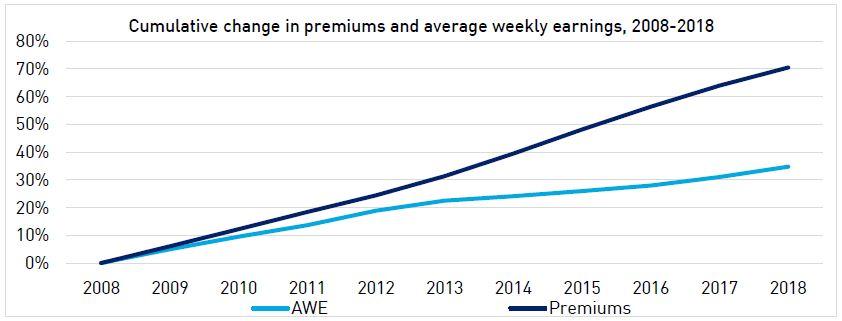

The industry is facing heightened pressures on a range of fronts. Higher demand for medical services by policyholders and increasing health costs are pushing premiums up. The resulting impact on affordability for policyholders is demonstrated in the following chart, which shows premiums have consistently grown faster than average weekly earnings over the last decade. Further, increasing out-of-pocket costs, changing consumer demands and the perception of low value are leading to a decline in the number of younger policyholders who play an important role in the sustainability of Australia’s community-rated system. Over the last decade, these pressures have contributed to an almost doubling of the proportion of insured persons who are aged 65 and over. These pressures are likely to continue into the foreseeable future.

While aspects of these sustainability risks are beyond the direct control of industry, APRA expects PHIs to be doing more than simply identifying these risks. In APRA’s view, sustainability pressures will continue to intensify for PHIs that do not take proactive steps to manage the impact of these risks. Consequently, APRA expects all PHIs to rapidly develop robust and actionable strategies to build resilience to these risks and engage regularly with APRA on the effectiveness of those strategies.

However, even well-developed strategies may not be successful, nor can they fortify PHIs against other events that impact solvency. Therefore, APRA also expects that all PHIs develop recovery plans to set out the actions they will take to respond to material risks that could threaten their solvency. Early preparation of recovery plans, including consideration of potential merger partners, will give PHIs more discretion when under pressure. In considering recovery actions, boards should ensure member interests always retain primacy. APRA will separately write to individual PHIs to provide guidance on expectations for an effective recovery plan.

Evidence from the review reiterates APRA’s consistent message to industry that PHIs with superior governance, business planning and risk management will be better placed to adapt to change and overcome threats. APRA’s review identified that PHIs better placed to manage sustainability risks had clear processes to monitor developments affecting their business. They used their risk management framework to analyse the impact of material risks and inform the board’s decisions on proactive responses. Further, APRA observed that responses more likely to be effective in mitigating the impact of these risks demonstrated:

- broader value for policyholders, including to meet the needs of younger and healthier members who are likely to value other services more highly than hospital treatment;

- managing claims costs by facilitating alternative models of care, as well as measures to support well-being and preventative health that assist policyholders in avoiding claims;

- and use of partnerships and outsourcing of material business functions to deliver better value for policyholders and manage costs.

The review found significant scope for improvement across the industry. For example, only one PHI had conducted quantitative analysis of a truly adverse affordability scenario. Further detailed observations from the review and APRA’s expectations for all PHIs are set out in Attachment A.

Inaction or inertia in the face of these challenges is likely to result in negative outcomes for PHIs and policyholders. A PHI that continues to take a passive approach to these risks can expect a more assertive response from APRA via entity-specific supervisory action to protect policyholders and the stability of the industry as a whole.

APRA supervisors will be working with PHIs on these matters over the coming period and will be challenging PHIs to make material improvements in their approach to managing these risks.

Yours sincerely,

Geoff Summerhayes

APRA Member

Attachment A: Observations and expectations from APRA's review of PHI resilience

Over the last few years APRA has become increasingly concerned about heightened risks facing the private health insurance industry. Affordability risk is becoming more pronounced as premiums continue to rise faster than wages and as a consequence there is reduced participation by policyholders, particularly younger and healthier Australians. At the same time, PHIs face risks in adapting to government policy changes designed to respond to pressure on the wider healthcare system. These sustainability risks in private health insurance pose challenges to traditional business models of PHIs and, if not well managed, have may have negative implications for policyholders with respect to PHI sustainability.

In response to this increasing concern, APRA commenced a review of PHI resilience in mid-2018 to get a better understanding of whether PHIs were adequately prepared to manage these risks. The review was also intended to inform APRA’s action to protect the interests of policy holders in the face of heightened risks to sustainability.

APRA assessed the readiness of 15 PHIs, chosen to provide a representative sample across the industry. The review included the five largest PHIs and a selection of smaller PHIs, with the sample covering both open and restricted membership PHIs as well as for-profit and not-for-profit PHIs. The review included those PHIs that appeared to be more proactive in managing these risks.

In conducting the review, APRA considered information from board reports, risk registers, scenario and financial analysis and any other documents related to the assessment and management of these issues.

The review assessed each PHI’s approach to:

- Its awareness of these issues, including the extent the issues were incorporated in risk registers, risk management plans, strategic plans and board reporting.

- The depth of assessment, in particular how the PHI assessed these issues, the view on severity, impact on the business, potential ways the risks could materialise and any scenario analysis completed.

- Strategy to manage these risks, including whether the PHI had a clear strategy, the detail of the strategy including responsibilities and governance, the PHI’s view on effectiveness and an assessment of its likely success.

- Actions taken to date, including the extent to which the strategy had been implemented, the success of the strategy to date, reporting, milestones and governance on actions taken.

The findings of the review are below, along with APRA’s expectations for PHIs to enhance their resilience to manage these risks.

1. Awareness

There was consistently strong awareness of the sustainability challenge posed by affordability and government policy change risks across the industry, with both risks being identified in almost all PHI's risk registers. PHIs demonstrated a strong understanding of the causes and most considered them among the biggest challenges facing their business.

PHIs demonstrated differing practices for the monitoring of these issues. Some entities had established clear processes to help them keep informed of developments, understand the impact on their business and regularly review the PHI’s strategy. Other PHIs had less structured approaches, with the board and other decision-makers being informed by infrequent updates, for example at an annual planning day or in passing references in other reports.

PHIs that demonstrated greater awareness were those that had established internal work streams to monitor industry developments, nominated key responsible people and disseminated this knowledge throughout the organisation. APRA observed better practices within those PHIs that are monitoring and disseminating information on a regular basis, drawing from a variety of sources that represent different perspectives including those of consumers, PHIs, regulators and suppliers.

1.1. That PHIs formalise the process that will be used to keep them informed of changes in the environment, including considering the timeliness of reporting to the board on how these could impact the PHI and whether the PHI’s strategy remains appropriate to manage within the new environment.

2. Assessment

The review found all PHIs had assessed the impact of potential government action to impose a 2 per cent cap on premium increases. This assessment included a quantified stress test of the impact on profitability, capital and prudential position over the next two to three years.

However, APRA observed narrow consideration by PHIs of ways their business may be affected by other policy changes, and consequently limited testing of alternative policy change scenarios. This narrow perspective ignores the history of the industry in which a number of changes in government policy have had a significant impact on the expectations of policy holders, industry structure and profitability.

APRA observed that better assessments of government policy change risk by PHIs included broader thinking on how these risks may impact their business and the identification of a variety of alternative scenarios for policy change. These assessments were supported by quantitative analysis of the impact of these scenarios at meaningful severities to examine the impact on capital and the profitability of the PHI. PHIs that demonstrated a higher level of engagement with the risks, as evidenced by deeper assessments were also found to have better strategies in place for addressing them.

There was less emphasis among PHIs on assessing the impact of affordability risk relative to the emphasis placed on the assessment of the impact of a cap on premium increases. This imbalance in assessment does not match industry’s own recognition of the importance of both risks.

In terms of affordability risk, the review found that PHIs had typically assessed the impacts in qualitative terms only, with few PHIs conducting quantitative analysis of an affordability scenario. For PHIs that did quantify the scenario, in all but one PHI the scenarios considered were benign, in that they did not stress the PHI. The review found that only one PHI had prepared an adverse affordability scenario. The disregard for assessing severe affordability stress scenarios is out-of-step with industry’s own view of the significance of the risk.

Better practice involved PHIs more severely stressing key risks. The boards of PHIs that are presented with analysis that challenges the core business are more likely to take the risk seriously, understand the implications of the risk and be able to make decisions on a more effective response. In APRA’s view, PHIs that quantify ‘extreme’ events as only having a low impact are less likely to effectively manage the issue.

Similarly, it is APRA’s view that PHIs that conducted a more credible qualitative assessment of affordability risk included the views of multiple stakeholders including various policy holders, health providers, other PHIs, industry groups and Government. Robust assessments were more detailed and demonstrated an understanding of the root cause of issues, highlighted areas to monitor and areas where the PHI could take action.

2.1. That PHIs stress test the most material risks in their risk register. Scenarios should demonstrate how risks could materialise, stress the business model at meaningful severities and assess the likely impact of mitigation strategies.

2.2. The scenarios should consider a variety of alternative scenarios for policy change, across different calibrations and be over a time horizon sufficiently long to stress the business and assess the long-term impact of mitigating strategies.

3. Strategy

APRA assessed the extent of each PHI’s strategy to address sustainability risks. These strategies were evaluated on their likelihood to be effective in boosting resilience. APRA observed that the majority of strategies were still at a very early stage of development. For example, many PHIs were yet to formalise and document implementation plans. APRA frequently observed a heavy reliance on industry associations, and many assumed the Government would take responsibility to address these risks.

A number of PHIs had also assessed their own strategy as likely to be ineffective, showing little to no difference between the risk impact before and after the PHI’s management of these risks. A credible strategy would involve the assessment of proposed actions to verify that those actions would meaningfully mitigate risk and a plan to monitor effectiveness. A credible strategy would also include the development of a recovery plan for if those actions were less effective than expected. Waiting for Government to ‘serve-up a solution’ is not a defensible strategy. In APRA’s view, policy holders are not well served by PHIs that defer action to others or that disregard their own responsibility to take steps to address these risks.

APRA observed strategies more likely to build resilience to Government policy changes are those that develop specific insurance offerings that provide value to policy holders while meeting the objectives of government. Better prepared PHIs were also observed to be using their expertise and data to conduct scenario analysis that informed the board’s strategic decisions, and could also be used to inform policy solutions that can be proposed to Government. PHIs that followed this approach had proactive strategies that were not solely reliant on the Government to change policy or increase funding for the sector.

APRA observed that more credible strategies to address affordability risks included a clear overall purpose, specific deliverables, responsibilities and timings. Typically, PHIs demonstrating these practices were informed by a robust assessment of the risks, feedback from policy holders and had strategies that involved various actions to address each underlying issue.

Better prepared PHIs were observed to be those making active efforts to adjust their business to reduce, rather than absorb the impact of affordability risk. Strategies observed in the review, included negotiation of supplier contracts to exert control over their claims costs, facilitating substitutes to in-hospital care, use of outsourcing and partnerships to achieve strategic objectives and participation in the delivery of medical services. The most effective strategies also demonstrated value to all policy holders, enhancing the customer experience by providing preventative health and well-being advice, increasing touch-points with policy holders and developing new product offerings that cater to policyholder interests.

PHIs with more robust strategies provide value to all policy holders and demonstrate two key characteristics:

- A focus on providing more cost-effective measures for delivery of medical services.

- A focus on providing services of value to all policy holders, especially to those who are younger and healthier and may not require hospital treatment.

3.1. That PHIs develop robust and proactive strategies to manage these risks, taking into account the perspectives of a range of stakeholders.

3.2. That PHIs assess whether their proposed actions would meaningfully mitigate the risks, and consider whether mitigation could be strengthened through outsourcing or strategic partnerships.

3.3. That PHIs develop a recovery plan for how they will respond should their strategy not be successful.

4. Actions taken

Where PHIs had a developed and documented strategy to address risks, these were generally at the early stage of implementation. The review found pilot programs are being trialled and monitoring metrics are still being built. For PHIs that are further progressed, APRA observed that in a number of cases it has taken several years to develop and implement such programs.

While not widely available, the review found tangible evidence of the cost savings achieved, benefits provided to policy holders and additional value created. This evidence was typically observed from PHIs that had established clear governance and responsibilities for the monitoring of strategy implementation and deliverables.

Better practice implementation was observed where PHIs had assigned risk owners with responsibility for monitoring implementation progress and were monitoring performance against clear metrics for strategy effectiveness. These entities also demonstrated an iterative approach to implementation by assessing effectiveness and reviewing strategy accordingly.

4.1. That PHIs have clear responsibility assigned for the development and implementation of these strategies. These strategies should articulate milestones with defined metrics and trigger points, along with governance and monitoring practices. This should be reported to the PHI’s board.

Footnotes

1 Health insurer, heal thyself: APRA’s prescription for financial sustainability, speech to the Members Health Directors’ Professional Development Program, February 2018.

Media enquiries

Contact APRA Media Unit, on +61 2 9210 3636

All other enquiries

For more information contact APRA on 1300 558 849.

The Australian Prudential Regulation Authority (APRA) is the prudential regulator of the financial services industry. It oversees banks, mutuals, general insurance and reinsurance companies, life insurance, private health insurers, friendly societies, and most members of the superannuation industry. APRA currently supervises institutions holding around $9 trillion in assets for Australian depositors, policyholders and superannuation fund members.