Crypto-assets: Risk management expectations and policy roadmap

In recent years, there has been rapid growth in crypto-assets and the use of distributed ledger technology. While activities associated with crypto-assets are still relatively limited in Australia, the potential scale and risks of such activities could become significant over time.

In this context, APRA is setting out initial risk management expectations for all regulated entities that engage in activities associated with crypto-assets, and a policy roadmap for the period ahead.1 Regulated entities should engage with their responsible supervisor if they are undertaking activities associated with crypto-assets.

APRA’s expectations regarding risk management

There are several types of crypto-assets, including tokenised traditional assets, crypto-assets with stabilisation mechanisms (stablecoins) and other unbacked crypto-assets, and a range of direct and indirect activities associated with these assets that entities could undertake. Such activities include, for example, investment in crypto-assets, lending linked with crypto-assets, issuance of crypto-assets, and providing services associated with crypto-assets for customers. In addition, entities may seek to invest in or partner with technology or other companies to provide new offerings for customers.

While these activities can provide opportunities and benefits for the financial system and its customers, they also bring new risks that may be challenging for entities to identify, assess and manage. As the Basel Committee on Banking Supervision has noted, certain crypto-assets have exhibited a high degree of volatility and could present material risks as exposures increase. The risks are wide-ranging, covering, for example, operational, investment, and credit risk. The operational risks are particularly important, and encompass fraud, cyber, conduct, AML/CTF and technology risks.

APRA therefore expects that all regulated entities will adopt a prudent approach if they are undertaking activities associated with crypto-assets, and ensure that any risks are well understood and well managed before launching material new initiatives.

In particular, APRA expects that all regulated entities will:

- Conduct appropriate due diligence and a comprehensive risk assessment before engaging in activities associated with crypto-assets, and ensure that they understand, and have actions in place to mitigate, any risks that they may be taking on in doing so;

- Consider the principles and requirements of Prudential Standard CPS 231 Outsourcing or Prudential Standard SPS 231 Outsourcing when relying on a third party in conducting activities involving crypto-assets; and

- Apply robust risk management controls, with clear accountabilities and relevant reporting to the Board on the key risks associated with new ventures.2 A high-level summary of the potential prudential risks to be considered for specific activities is provided in Annex A.

Entities also need to ensure they comply with all conduct and disclosure regulation administered by ASIC. This will require robust conduct risk management and consideration of distribution practices and product design, as well as consideration of disclosure.

Entities are expected to consult with APRA and ASIC where they are unclear on prudential, disclosure or conduct requirements and expectations when undertaking activities associated with crypto-assets. ASIC has provided specific guidance to help entities understand their existing obligations under the Corporations Act and ASIC Act in ASIC Information Sheet 225.

Policy roadmap

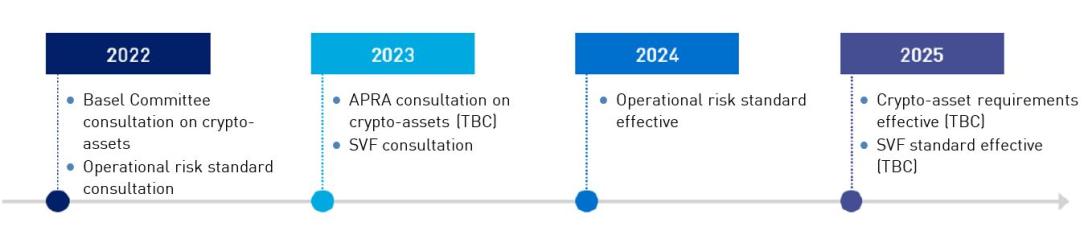

APRA is developing the longer-term prudential framework for crypto-assets and related activities in Australia in consultation with other regulators internationally, to ensure consistency in approach. For authorised deposit-taking institutions (ADIs), the Basel Committee is consulting on the prudential treatment for bank exposures to crypto-assets.3 This will provide the basis for internationally agreed minimum standards for ADIs, and a starting point for prudential expectations for other APRA-regulated industries.

In the period ahead, APRA plans to:

- crypto-activities: consult on requirements for the prudential treatment of crypto-asset exposures in Australia for ADIs, following the conclusion of the Basel Committee’s current consultation. The consultation in Australia is expected to be undertaken in 2023, and APRA will consider the need for initial prudential guidance in the interim;

- operational risk: progress new and revised requirements for operational risk management, covering control effectiveness, business continuity and service provider management. While these requirements will apply to the entirety of an entity’s operations, many will be directly relevant to the management of operational risks associated with crypto-asset activities. The draft prudential standard will be released for consultation in mid-2022; and

- stablecoins: consider possible approaches to the prudential regulation of payment stablecoins. These stablecoin arrangements bear similarities with Stored-value Facilities (SVFs) and APRA, in conjunction with peer agencies on the Council of Financial Regulators (CFR), is developing options for incorporating them into the proposed regulatory framework for SVFs. Subject to the development of the broader legislative and regulatory framework, APRA envisages consulting on prudential requirements for large SVFs in 2023.4

As set out in Transforming Australia’s Payments System in December 2021, and subject to any decisions of an incoming government, there will also be a range of developments in the regulatory framework for crypto-assets and payments more broadly in the period ahead. This follows several key reports in 2021, including the Review of the Australian Payments System, the Senate Committee on Australia as a Financial and Technology Centre Final Report, and the Parliamentary Joint Committee Corporates and Financial Services Report on Mobile Payment and Digital Wallet Services. As part of these broader reforms, the Treasury recently released a consultation on proposed licensing and custody requirements for crypto asset secondary service providers, including digital currency exchanges.5

APRA will continue to closely monitor industry trends and emerging risks associated with crypto-assets, engage with other regulators domestically and internationally, and provide further guidance as required.

Yours sincerely,

Wayne Byres

Chair

ANNEX A. prudential risks and relevant standards

The table below sets out an initial view on the potential prudential risks for crypto-asset activities relevant to APRA-regulated industries. This risk assessment will evolve over time.6

Activities | Prudential risks |

|---|---|

Investments in crypto assets |

|

Lending activities linked with crypto assets |

|

Crypto assets issuance |

|

Services on crypto assets for customers |

|

Partnering with technology and other companies |

|

Footnotes:

- APRA outlined a new strategic initiative to Modernise the Prudential Architecture in its Corporate Plan for 2021-2025. The aim of this initiative is to ensure that the prudential framework continues to support financial safety and stability in a digital world, including through new rules for new risks such as those arising from crypto-assets. For more detail on the broader plans to modernise the architecture, see APRA’s Policy Priorities (February 2022).

- For an ADI, APRA expects that the accountabilities for crypto-asset activities would be assigned to a BEAR Accountable Person(s), with adjustments to their accountability statements where appropriate. Entities should consider the impact of all new products on their operational risk profile, and implement any changes required to internal controls.

Basel Committee on Banking Supervision, Consultation on the Prudential treatment of crypto-asset exposures (June 2021).

Payment stablecoins have features that enable them to be used as a possible means of payment and store of value. The proposed SVF framework was published by the CFR in November 2020 and is expected to be implemented as part of the Government's reforms to the payments licensing framework announced in December 2021. APRA’s existing requirements for Purchased payment facility providers that have stored value at risk are set out in Prudential Standard APS 610 Prudential Requirements for Providers of Purchased Payment Facilities (APS 610).

Crypto asset secondary service providers: Licensing and custody requirementsconsultation paper (21 March 2022).

This table outlines potential key risks to consider, but the specific risks will depend on the nature of the activity. Prudential Standard CPS 220 Risk Management defines material risks as encompassing: credit risk, market and investment risk, liquidity risk, insurance risk, operational risk, risks arising from strategic objectives and business plans, and other risks that may have a material impact on the entity.

Prudential Standard APS 111 Capital Adequacy: Measurement of Capital, Prudential Standard GPS 112 Capital Adequacy: Measurement of Capital, Prudential Standard LPS 112 Capital Adequacy: Measurement of Capital.

Refer to s. 52(2)(c) of the Superannuation Industry (Supervision) Act 1993 (SIS Act), s. 52(6) of the SIS Act and Prudential Standard SPS 530 Investment Governance respectively.

Prudential Standard APS 220 Credit Risk Management includes requirements for collateral valuation, as well as for credit risk management more broadly.

Prudential Standard APS 111 Capital Adequacy: Measurement of Capital, Prudential Standard GPS 112 Capital Adequacy: Measurement of Capital, Prudential Standard LPS 112 Capital Adequacy: Measurement of Capital.

Prudential Standard CPS 231 Outsourcing, Prudential Standard SPS 231 Outsourcing.

For more information

- If you are from an APRA supervised institution, contact your APRA Responsible Supervisor.

- All other users should contact APRA on 1300 558 849 or complete our enquiries form.