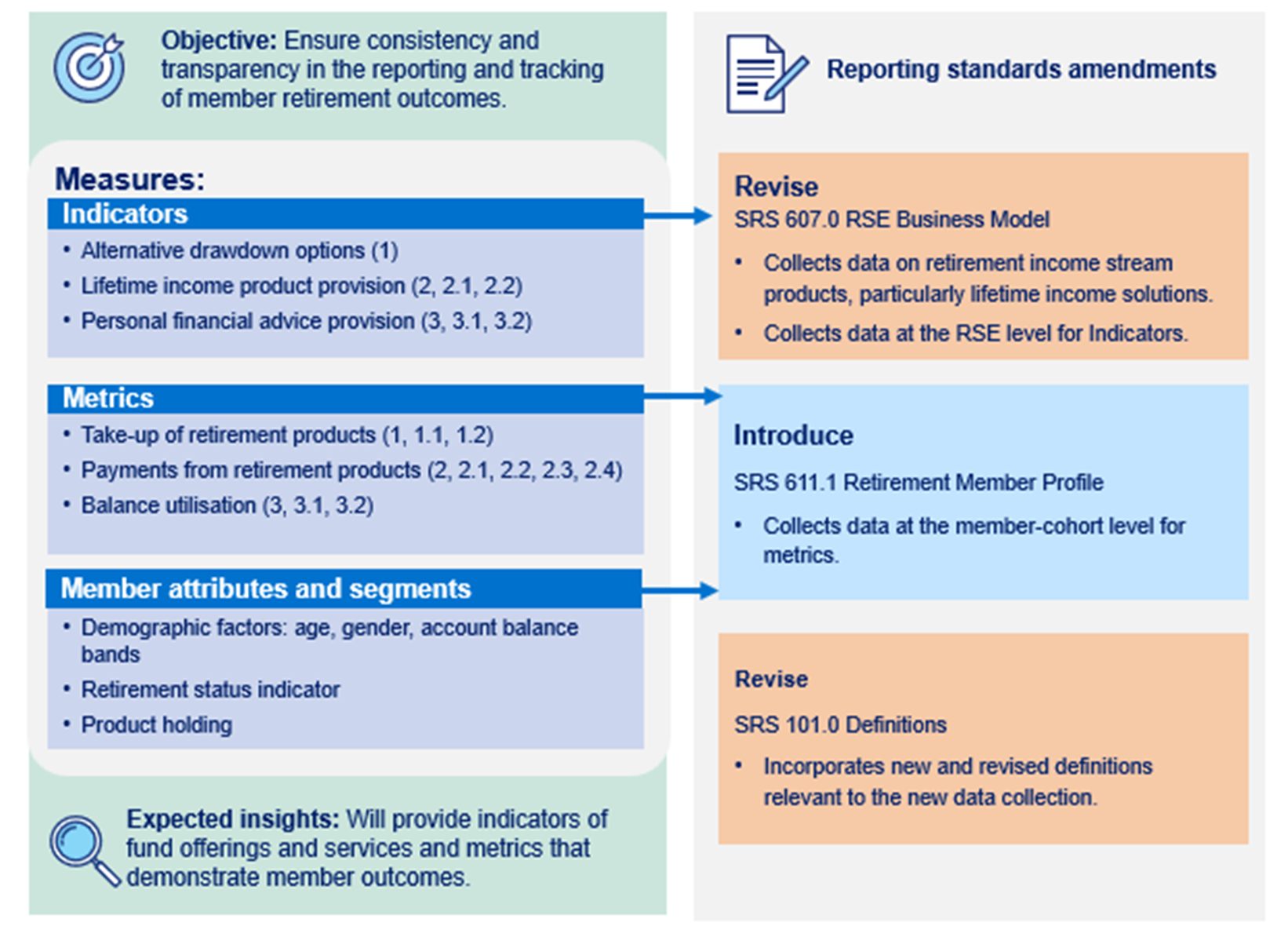

Incorporating the member attributes listed in the Framework Design Specifications into the data collection will provide additional contextual information to the Framework’s metrics.

The draft reporting standard SRS 611.1 Retirement Member Profile collects data at a member-cohort level. For this purpose, each unique combination of the member attributes – age, gender, account balance band, retirement status indicators, and member product holdings or actions – creates a member-cohort.

Structuring the collection of member-cohort level data in this way enables the metrics to be calculated in a consistent way for industry-level, RSE-level, as well as with reference to relevant member attributes.

In proposing this approach to member-cohorts, the working assumption is that it will increase the amount of data submitted annually but will not necessarily be a material driver of regulatory impact and cost. Through the consultation process, APRA welcomes feedback on this aspect specifically.

For some metrics, not all attributes are applicable. See the technical paper for further information.

Sections 1.4.1 through 1.4.5 provide further information on how the attributes are defined. APRA has aligned these attributes to existing reporting standards wherever possible. Further detail is set out below on the adjustments proposed for account balance bands and types of products, and the introduction of the concept of retirement status indicators.

1.4.1 Age

The Framework is focused on members who are 60 years of age and above. To maintain consistency with APRA’s approach in other standards (e.g. SRS 611.0), APRA proposes data will be collected for each individual age from 60 years of age and above. Individual ages, rather than an age band approach provides the detail needed to track how key age-related milestones, such eligibility for the Age Pension, may impact on member behaviour throughout the retirement journey.

1.4.2 Gender

APRA proposes to collect sex type according to four categories; female, male, other, not stated or inadequately described. This adopts the approach used in APRA’s existing standards (e.g. SRS 611.0), which also aligns with the Australian Bureau of Statistics standard for the collection of data relating to sex, gender, variations of sex characteristics and sexual orientation variables.

1.4.3 Account balance bands

To segment members according to their account balance, APRA proposes to use the same approach as applied in SRS 611.0 with some minor adjustments. Currently SRS 611.0 collects member benefits via twelve brackets as set out in Table 3 below. In the proposed SRS 611.1 collection, APRA has maintained twelve brackets but adjusted the boundaries to better reflect the distribution of member benefits for members at or in retirement. The bands suggested are expected to allow for a more uniform distribution of data, while still allowing some comparison of member data between SRS 611.0 and SRS 611.1. The comparison between SRS 611.0 and proposed SRS 611.1 is shown in the table below.

Table 3. Proposed members' benefits brackets

Bracket No # | Current

Members benefit brackets in SRS 611.0 | Bracket No # | Proposed

Members benefit brackets for SRS 611.1 |

|---|

1 | <$1,000 | 1 | <$1,000 |

2 | $1,000 - $5,999 | 2 | $1,000 - $5,999 |

3 | $6,000 - $9,999 | 3 | $6,000 - $14,999 |

4 | $10,000 - $14,999 |

5 | $15,000 - $24,999 | 4 | $15,000 - $24,999 |

6 | $25,000 - $39,999 | 5 | $25,000 - $59,999 |

7 | $40,000 - $59,999 |

8 | $60,000 - $99,999 | 6 | $60,000 - $99,999 |

9 | $100,000 - $199,999 | 7 | $100,000 - $199,999 |

10 | $200,000 - $499,999 | 8 | $200,000 - $349,999 |

9 | $350,000 - $499,999 |

11 | $500,000 - $999,999 | 10 | $500,000 - $999,999 |

12 | $1,000,000+ | 11 | $1,000,000 - $1,999,999 |

12 | $2,000,000+ |

1.4.4 Retirement Status indicators

APRA proposes to use certain behaviours or actions taken by members as a proxy – or indicator – for members’ retirement status. These are considered appropriate proxies given the complexity industry otherwise faces in identifying members’ actual retirement status.

As set out below:

- Not yet retired – members who are 60 years and above as at the end of the reporting period; who held only an accumulation (or transition to retirement account) at the start and end of the reporting period; and, have not taken a lump sum withdrawal during the reporting period, will be categorised as part of the ‘not yet retired’ member segment. This member segment will be collected within SRS 611.1 Table 2.

- Retired during reporting period - members who are 60 years and above as at the end of the reporting period, and who held only an accumulation (or transition to retirement account) at the start of the reporting period, but commenced a retirement income stream product or received a lump sum withdrawal during the reporting period categorised as part of the ‘retired during reporting period’ member segment. This member segment will be collected within SRS 611.1 Table 2.

- Retired in prior reporting period - members who are 60 years and above as at the end of the reporting period, and who held an account-based pension (or allocated pension) at the start of the reporting period will be categorised as part of the ‘retired in prior reporting period’ member segment. This member segment will be collected within SRS 611.1 Table 3.

APRA welcomes feedback on practicable alternative approaches to collecting indicators of retirement status that would not impose additional reporting burden.

1.4.5 Product Holdings

APRA proposes limiting the number of retirement product type categories included in the collection to the five product types listed below:

- Accumulation products

- Transition to retirement pensions

- Account-based pensions (allocated pensions will also be reported within this category)

- Lifetime income products

- Other retirement income streams – includes a range of other income streams including term annuities

These categories are updated from SRS 610.0 to reflect changes in regulatory settings and the focus of the Framework. For example, account-based pensions and allocated pensions are separately recorded in 610.0 but APRA proposes to combine these into one category in SRS 611.1 reflecting that allocated pensions have been largely superseded by account-based pensions.

SRS 610.0 collects data on annuities via a standalone category, whereas in SRS 611.1 the new category of lifetime income products will capture annuities that meet the conditions of providing a lifetime income. Deferred income streams not in the retirement stage, will be classified as an accumulation product for the purposes of this collection. Once a deferred lifetime income stream is in the retirement phase, it will be classified as a lifetime income product, even where the income payments have been deferred. Annuities which do not meet the condition of providing lifetime income – such as term annuities – will be categorised into ‘other’ retirement income streams in SRS 611.1.

APRA invites comments from RSEs regarding these categorisations, specifically if there is a need to separately report any retirement income streams – such as term annuities – that are consolidated into the other retirement income stream category.

1.5 Key design choices to minimise regulatory impact

In order to minimise unnecessary impact on industry from this new collection, APRA has sought to achieve coherence with existing APRA and broader reporting requirements. Specifically, APRA has wherever possible drawn upon definitions and data fields already used to fulfil other reporting requirements, including within APRA and Services Australia Automation of Income Stream Review reporting requirements.

APRA considered the suitability of a range of existing APRA collections (including SRS 332.0, SRS 605.0, SRS 610.0, SRS 610.1, SRS 710.0) to fulfil the Framework. APRA has determined restructuring those existing standards to meet the requirements of the Framework would have a greater impact on industry than the proposed approach to amend SRS 607.0, introduce SRS 611.1 and revoke SRS 610.0 (refer Table 1 and 2 for more detail).

In a number of instances, APRA has proposed proxies for certain data fields (such as balance at death) or attributes (such as retirement status indicators) to reduce the complexity of otherwise trying to capture specific data points. The technical paper provides more detail on the methodology proposed for each metric.

In considering the large range of product types that may be held by members in retirement, subject to consultation feedback, APRA proposes that only product types that are widely held or are a specific focus of the Framework (for example lifetime income products) will be separately reported. Retirement products held by a small number of members will be reported under one consolidated product type category (i.e. other retirement income streams), to help reduce the complexity of the collection.

To structure the collection according to the member cohorts set out in the Framework, APRA has proposed an approach that seeks to minimise the need for industry to make changes to existing practices. This is discussed further in section 1.4.

Finally, APRA engaged with the Australian Taxation Office (ATO) to test the feasibility of drawing on ATO data to inform the Framework. However, APRA’s assessment is that the data collected by the ATO is unable to be used for the indicators and all of the metrics. A hybrid approach is not expected to be suitable.

2. Proposed publication of data

APRA’s proposed approach to publication is set out below. APRA has combined the consultation on the reporting standards with the consultation on the publication to reduce burden on industry.

2.1 Data publication

Publication of data is a key intended purpose of data collection, as set out in Government announcements and the Framework Design Specifications. The annual publication is intended to improve consistency and transparency in the reporting and tracking of member retirement outcomes.

APRA is seeking to take a balanced approach to publication, publishing data that is meaningful and fit-for-purpose for industry and broader stakeholders, while also being mindful of commercial and privacy considerations.

APRA’s high-level approach to inaugural publication in 2028 is summarised in the table below.

Table 4. Summary of proposed approach to inaugural publication in 2028

| Publication scope and parameters | Summary of proposed approach to inaugural publication in 2028 |

|---|

| Scope of publication | 1. At an RSE level, each of the indicators, including drawdown options, lifetime income products and personal advice services. - For indicators 1, 2, 2.1 and 3, the published outcome will be a Yes or No response for each RSE.

- For indicator 2.2, APRA proposes to categorise and publish the types of lifetime income products provided through each RSE.

- Indicators 3.1 and 3.2, which consider the take-up of specified categories of personal financial advice, will be published at the RSE level as an overall proportion of members aged 60 or over who received the defined personal financial advice.

2. At an RSE level, each of the metrics, including types of retirement products held by members, drawdown levels and value of benefit payments, balance utilisation and actions taken. 3. At an RSE level, each of the metrics, segmented by up to two or three different member attributes (e.g. by age and gender, or account balance bands and product holdings, etc). 4. For the above items APRA will also consider what is appropriate to publish at an industry level. 5. Accessible format to align with transparency focus. |

| Parameters for publication | - At a high-level, comparable level of aggregation to APRA’s existing publications. APRA is not proposing publication of data at the same level reported to APRA.

- In particular, application of existing APRA data masking protocols (e.g. in relation to small number of members) to safeguard confidentiality of member information.

|

APRA welcomes feedback from stakeholders, including regarding the data that would be valuable to include in the publication, as well as any commerciality or privacy considerations APRA should bear in mind.

APRA anticipates the publication of data will evolve in future years, however, where changes are proposed APRA would consider the need for further consultation where changes are material in nature.

APRA intends to publish fund level reporting of the Framework indicators and metrics, with minimal additional calculations such as converting dollar values into percentages.

For detail on how the Framework’s indicators and metrics will be calculated for publication, refer to the accompanying technical paper.

2.2 Confidentiality proposal

APRA proposes to determine the data to be collected under the proposed collection to be non-confidential under s57 of the APRA Act, with publication of the data subject to and consistent with the principles outlined above. Existing APRA data masking protocols to safeguard confidentiality of member information will be applied.

APRA is providing RSE licensees and other interested parties with an opportunity to make representations as to whether the reporting collection proposed to be declared non-confidential contains confidential information.

3. Consultation process and questions

3.1 Request for written submissions

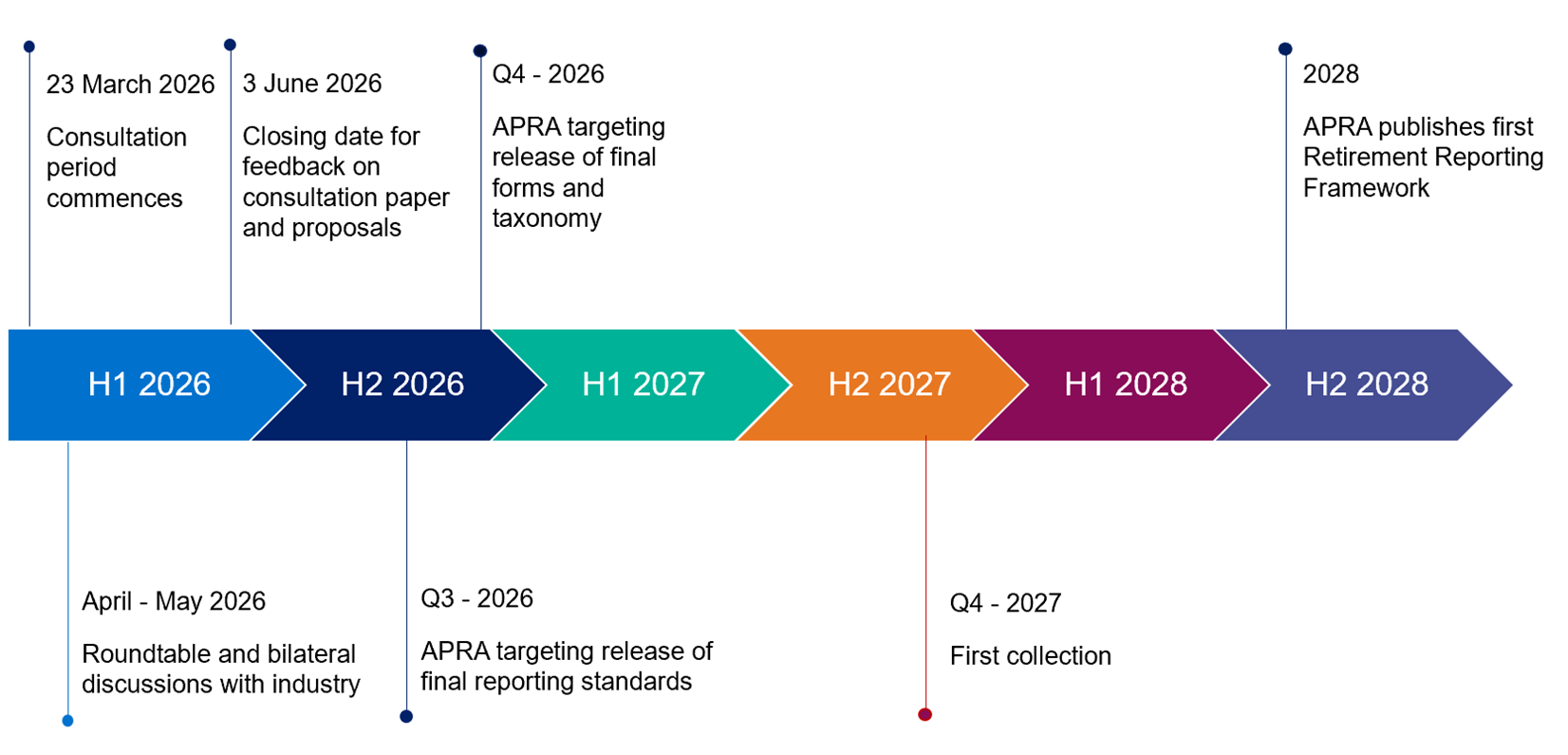

APRA invites written submission on the proposals set out in this consultation paper by 3 June 2026.

Written submissions should be emailed to RetirementDataConsultation@apra.gov.au and addressed to:

General Manager

Branch 4

Life, Private Health Insurance and Superannuation Division

Australian Prudential Regulation Authority

GPO Box 9836 SYDNEY NSW 2001

3.2 Request for regulatory burden impact information

APRA asks that all stakeholders use this consultation opportunity to provide information on the compliance impact of the proposals, and any other substantive costs including business costs. Compliance costs are defined as direct costs to businesses of performing activities associated with complying with government regulation. Specifically, information is sought on any changes to compliance costs incurred by businesses as a result of APRA’s proposals.

Consistent with the Government’s approach, APRA will use the methodology behind the Regulatory Burden Measurement Framework to assess compliance costs. It is available at Regulatory Burden Measurement Framework.

APRA requests that respondents use this methodology to estimate costs to ensure the data supplied to APRA can be aggregated and used in an industry-wide assessment. When submitting cost assessments to APRA, respondents should include any assumptions made and, where relevant, any limitations inherent in their assessment. Feedback should address the additional costs incurred as a result of complying with APRA’s requirements, not activities that institutions would undertake due to foreign regulatory requirements or in their ordinary course of business.

3.3 Consultation questions

APRA requests that stakeholders structure feedback with reference to the following set of questions.

Regulatory Balance

- Does the proposed approach effectively implement the Government’s Framework as announced on 23 February 2026, including meeting the Framework Design Specifications?

- How feasible is it to collect and report this data? Are there any material impediments to doing so?

- What are the changes to compliance costs as a result of the proposals? Please identify elements or approaches that have the greatest impact on regulatory burden? (refer to section 3.2 above for further detail)

- Given the intent of collecting data in late 2027, is the proposed timeline achievable?

- In your view, does the proposed approach strike an appropriate regulatory balance? Are there specific alternative approaches that you would recommend be considered? Where an alternative approach or option is recommended, please separately identify the difference in compliance costs.

- What is the estimated quantum of data (e.g. rows per table) expected to be reported?

Would there be significant value collecting more information:

7.1 in relation to financial advice, for example segmenting indicator 3 by member cohort or attributes?

7.2 in relation to retirement income streams, for example by capturing term annuities separately from the ‘other retirement income stream category’?

Confidentiality

- Considering APRA’s proposal to publish data in 2028, are there any specific data items that should be considered confidential and/or commercially sensitive?

Publication

- What further measures could APRA adopt to enhance the transparency and accessibility of the annual Framework publication?

- What factors should APRA consider when deciding which member-cohort level data to release, publish, or aggregate?

Technical aspects

Do you have any comments on the proposed technical design, including in relation to:

11.1 Defining and categorising product types (section 2.2.5, and SRS 101)?

11.2 Revocation of SRS 610.0 (section 2.4.1)?

11.3 Formulas to calculate metrics (Technical paper)?

- Will the use of the proposed proxy for retirement status indicators result in meaningfully accurate results? Are there alternative proxies APRA should consider?

- Are the definitions and guidance in the reporting instructions sufficiently clear?

3.4 Important disclosure requirements - publication of submissions

All information in submissions will be made available to the public on the APRA website unless a respondent expressly requests that all or part of the submission is to remain in confidence. Automatically generated confidentiality statements in emails do not suffice for this purpose. Respondents who would like part of their submission to remain in confidence should provide this information marked as confidential in a separate attachment.

Submissions may be the subject of a request for access made under the FOIA. APRA will consider and determine such requests, if any, in accordance with the provisions of the FOIA. Information in the submission about the affairs of any financial sector entity (including an APRA-regulated entity) that is not in the public domain and that is identified as confidential will be protected by section 56 of the APRA Act and will therefore, subject to limited exemptions, be exempt from production under the FOIA.

3.5 Data security

APRA regards maintaining the security of entity data as the highest priority.

APRA is governed by the Protective Security Policy Framework, which outlines required governance, protective, detective and response security capabilities. A security risk management practice is in place to assess cyber security risks, covering the availability, confidentiality and integrity of data and systems.

APRA applies the Australian Cyber Security Centre Information Security Manual (ACSC ISM), which includes the Essential Eight mitigation strategies. The ACSC ISM provides guidance for cyber security roles and incidents, procurement and outsourcing, security documentation, physical security, personnel security, communications infrastructure, communications systems, enterprise mobility, evaluated products, ICT equipment, media, system hardening, system management, system monitoring, software development, database systems, email, networking, cryptography, gateways and data transfers.

Annexure: Government Framework Design Specifications

Note: In February 2026, the Government announced the finalisation of the Framework and released a factsheet outlining the final design specifications (Framework Design Specifications). With the agreement of the Australian Treasury, the factsheet is hosted by APRA and referenced in this consultation paper. It is available in full as a PDF on APRA’s website at: Treasury - Retirement Reporting Framework Factsheet.

Glossary

| Term | Definition |

|---|

| APRA Act | Australian Prudential Regulation Authority Act 1998 |

| Covenant | The retirement income covenant under s 52(8A) and 52(8B) of the SIS Act |

| FOIA | Freedom of Information Act 1982 |

| the Framework | The Retirement Reporting Framework |

| RSE | Registrable superannuation entity |

| RSE licensee | Registrable superannuation entity licensee as defined in s 10(1) of the SIS Act |

| SIS Act | Superannuation Industry (Supervision) Act 1993 |

| SRS 101.0 | Reporting Standard SRS 101.0 Definitions for Superannuation Data Collections |

| SRS 332.0 | Reporting Standard SRS 332.0 Expenses and Investment and Transaction Fees and Costs |

| SRS 605.0 | Reporting Standard SRS 605.0 RSE Structure |

| SRS 607.0 | Reporting Standard SRS 607.0 RSE Business Model |

| SRS 610.0 | Reporting Standard SRS 610.0 Membership Profile |

| SRS 610.1 | Reporting Standard SRS 610.1 Changes in Membership Profile |

| SRS 710.0 | Reporting Standard SRS 710.0 Conditions of Release |

| SRS 611.0 | Reporting Standard SRS 611.0 Member Accounts |

| SPS 515 | Prudential Standard 515 Strategic Planning and Member Outcomes |